Michigan Health Insurance: 2026 Plans, Costs & Coverage Guide

Michigan health insurance for 2026 is going through the most significant marketplace shakeup in more than a decade. Seven carriers now offer individual plans through HealthCare.gov — down from ten in 2025 — with Molina Healthcare, HAP CareSource, and the University of Michigan’s UM Health Plan all exiting the individual market. Michigan’s approved 2026 rate increase averages 20.1%, driven by carrier exits, the expiration of enhanced premium tax credits, and rising medical costs. This guide covers what’s available, what it costs, how Healthy Michigan Plan fills the low-income coverage gap, and how to choose among the remaining carriers.

What brings you to Michigan health insurance today?

The 2026 Michigan Marketplace Shakeup

Michigan’s 2026 individual market lost three carriers from the previous year: Molina Healthcare pulled out of both Michigan and Wisconsin entirely, HAP CareSource withdrew its approximately 18,800 enrollees from the marketplace, and Michigan Medicine dissolved its UM Health Plan (formerly Physicians Health Plan), displacing roughly 64,000 enrollees in the Lansing area. About 200,000 state residents could not renew with their prior carrier for 2026 — the most significant marketplace shakeup in more than a decade.

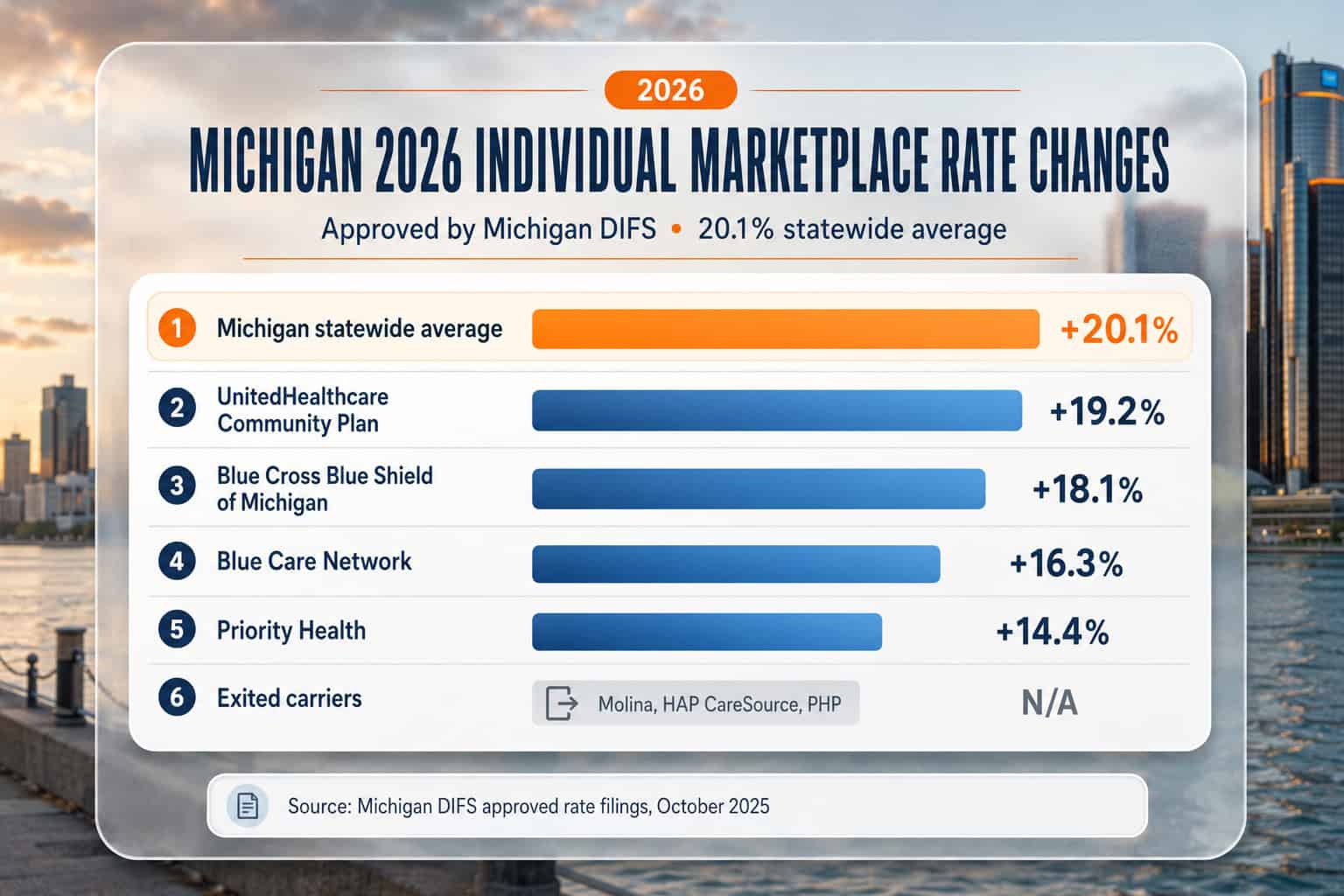

The remaining seven Marketplace carriers for 2026 are Blue Cross Blue Shield of Michigan, Blue Care Network of Michigan, Priority Health, Meridian Health Plan (Ambetter), McLaren Health Plan, Oscar Health, and United Healthcare Community Plan. Plan count dropped from 162 in 2025 to 116 for 2026, giving consumers fewer choices and, in many counties, only two or three carrier options. The Michigan Department of Insurance and Financial Services (DIFS) approved 20 filings covering 191 individual health plans total, with 116 appearing on HealthCare.gov and others available off-exchange.

If your 2025 carrier left the market: Former Molina, HAP CareSource, or UM Health Plan enrollees needed to actively enroll in a new plan on HealthCare.gov for 2026. There is no automatic renewal to a different carrier. Missing the Open Enrollment deadline without a Qualifying Life Event means waiting until the next enrollment window — a potentially costly coverage gap.

Michigan Health Insurance Carriers for 2026

Seven carriers offer health plans through HealthCare.gov for 2026. Blue Cross Blue Shield of Michigan and Blue Care Network together hold the largest market share statewide. Priority Health dominates western Michigan from its Grand Rapids headquarters. Meridian Health Plan (operating as Ambetter) serves southeast Michigan and the Detroit metro. Availability varies significantly by county — some rural counties have only two or three carrier options while Detroit metro residents typically see all seven.

| Carrier | 2026 Rate Change | Primary Region | Network Type |

|---|---|---|---|

| Blue Cross Blue Shield of Michigan | +18.1% | Statewide | PPO (broadest network) |

| Blue Care Network of Michigan | +16.3% | Statewide | HMO (BCBS HMO affiliate) |

| Priority Health | +14.4% | West Michigan, expanding | HMO and POS |

| Meridian (Ambetter) | Scaling back | Southeast Michigan | HMO |

| McLaren Health Plan | Varies by plan | Flint, central Michigan | HMO (McLaren system) |

| Oscar Health | Varies by plan | Detroit metro select | HMO |

| UnitedHealthcare Community Plan | +19.2% | Select counties | HMO |

Blue Cross Blue Shield of Michigan remains the state’s dominant carrier for good reason: it offers the only statewide PPO option on the Michigan marketplace, with the broadest provider network covering nearly every hospital and health system in the state. BCBS posted a 2024 underwriting loss of $1.7 billion and cited that loss as justification for the 18.1% rate increase. Blue Care Network — BCBS’s HMO affiliate — offers lower premiums ($460–$520/month Silver for a 40-year-old in Wayne County) with a narrower but still substantial network. The Michigan carrier comparison guide breaks down each carrier’s strengths and network reach in detail.

Priority Health, headquartered in Grand Rapids, is the dominant carrier in west Michigan — Kent, Ottawa, Muskegon, Allegan, and Kalamazoo counties — where it competes aggressively with BCBS on price and network. Priority’s 14.4% rate increase was the lowest among major Michigan carriers for 2026, making it a strong value option for west Michigan residents whose providers participate in the Spectrum Health / Corewell Health and Bronson Healthcare networks.

DALL-E prompt:

Filename: mi-pillar-carrier-rate-changes-2026.jpg

Tool: ChatGPT / GPT Image

Scene type: Data visual — horizontal bar chart

State anchor: Michigan — 2026 approved rate changes by carrier

═══ CONTENT ═══

Title: “Michigan 2026 Individual Marketplace Rate Changes”

Subtitle: “Approved by Michigan DIFS — 20.1% statewide average”

Layout: Horizontal bar chart with 6 bars, each carrier’s approved rate change, longest at top

Bar 1: Priority Health — +14.4%

Bar 2: Blue Care Network — +16.3%

Bar 3: Blue Cross Blue Shield of Michigan — +18.1%

Bar 4: UnitedHealthcare Community Plan — +19.2%

Bar 5: Michigan statewide average — +20.1% (highlighted)

Bar 6: Exited carriers (Molina, HAP CareSource, PHP) — N/A (marked with exit icon)

Footer line: “Source: Michigan DIFS approved rate filings, October 2025”

═══ DESIGN SYSTEM ═══

Premium Infographic System: soft shadows under bars, subtle bevel/edge lighting, consistent top-left light source, layered surfaces. Strong title hierarchy (bold, spaced, centered), clean numeric emphasis (percentage values larger and heavier), consistent row spacing. Card-based container with rounded corners and padding, grid-aligned bars. Minimal embedded indicators (a small icon for exited carriers).

Color treatment: Apply the brand primary color (teal-blue) as a gradient fill across the carrier bars. Apply the brand accent color (warm orange) to highlight the statewide-average bar (the benchmark the eye should land on). Supporting color: any single mid-tone color from the analogous blue-green/blue-violet families OR the triadic warm red/burgundy/mustard/gold families, medium-low saturation, used only for the exited-carrier bar or a subtle divider. Pair with a light cream or parchment background (not pure white). Do not select a supporting color that competes with the brand orange accent. Do not display any color name or color code on the image.

═══ HARD RULES (non-negotiable) ═══

• Exact dimensions: 1200×800px — no deviation

• No text overflow — all labels and callouts must fit inside the chart area with comfortable padding

• Proportional data scaling — bars must be proportional to their percentage values, aligned to the same baseline

• No spelling errors in any text — double-check every word

• No human subjects

• No flat grey tables, harsh outlines, or misaligned spacing

• No design specifications, color codes, RGB values, or prompting instructions may appear as visible text in the final image. Treat all color references as paint instructions, never as content.

How Much Does Michigan Health Insurance Cost in 2026?

Michigan health insurance premiums for 2026 average $486/month for a 40-year-old Silver plan before subsidies, up from approximately $405/month in 2025 — a 20.1% increase. After premium tax credits, 90% of Michigan marketplace enrollees pay significantly less: the average after-subsidy premium is approximately $106/month, reflecting subsidies that average more than $380/month per enrollee. Costs vary substantially by county, age, tobacco use, and carrier selection.

| Age | Bronze (40yo equiv) | Silver (40yo equiv) | Gold (40yo equiv) |

|---|---|---|---|

| 25 (Wayne County) | ~$285/mo | ~$390/mo | ~$510/mo |

| 40 (Wayne County) | ~$365/mo | ~$486/mo | ~$635/mo |

| 55 (Wayne County) | ~$735/mo | ~$980/mo | ~$1,280/mo |

| 62 (Wayne County) | ~$940/mo | ~$1,255/mo | ~$1,640/mo |

| 40 (Upper Peninsula) | ~$420/mo | ~$560/mo | ~$730/mo |

Michigan’s 20.1% rate increase reflects multiple compounding factors: the scheduled expiration of enhanced Premium Tax Credits from the American Rescue Plan and Inflation Reduction Act, the departure of three carriers (which concentrated risk among the remaining insurers), continued medical cost inflation, prescription drug price increases, and a BCBS of Michigan underwriting loss of $1.7 billion in 2024. For unsubsidized Michiganders — particularly those above 400% of the Federal Poverty Level — the full rate increase hits directly. A 62-year-old West Bloomfield attorney earning above the subsidy cliff can now face premiums exceeding $1,300/month for a full-price Silver plan.

For subsidized enrollees, the picture is different: because premium tax credits adjust to match the benchmark Silver plan, most of the rate increase is absorbed by the federal government rather than passed to the enrollee. A Wayne County resident earning $35,000 (about 233% FPL) typically qualifies for approximately $380/month in subsidies, bringing a Silver plan from $486/month to approximately $106/month. The affordable coverage guide details subsidy strategies by income level.

See Michigan Health Insurance Options for Your County

Compare 2026 plans from all seven Michigan marketplace carriers. Check subsidy eligibility, see after-subsidy pricing, and find coverage that fits your household budget.

Premium Tax Credits and Subsidies in Michigan

Approximately 90% of Michigan marketplace enrollees receive premium tax credits — one of the highest subsidy participation rates in the country. The average subsidy is approximately $380/month per enrollee. The state does not operate a supplemental subsidy program, so Michiganders rely entirely on federal premium tax credits and cost-sharing reductions. The scheduled expiration of enhanced subsidies under the American Rescue Plan and Inflation Reduction Act is a significant concern for about 40,000 Michigan families who would lose eligibility.

Premium tax credits work by capping the amount a household pays for the benchmark (second-lowest-cost) Silver plan as a percentage of income. Under the enhanced subsidies in effect through 2025, households earning up to 400% FPL paid no more than 8.5% of income for the benchmark plan, and households above 400% FPL also qualified if their benchmark premium exceeded 8.5% of income. Without Congressional extension, the pre-2021 subsidy structure returns — phasing out entirely at 400% FPL and creating a “subsidy cliff” that hits older Michiganders hardest.

Example: Wayne County Resident, $35,000 Income

A 40-year-old in Wayne County earning $35,000 per year (about 233% FPL) qualifies for roughly $380/month in premium tax credits in 2026. That brings a benchmark Silver plan from approximately $486/month down to about $106/month after the subsidy. Because the household is under 250% FPL, choosing a Silver plan also unlocks Cost-Sharing Reductions that lower the deductible and copays — making Silver the strongest value at this income level.

Subsidy cliff warning for 2026: If enhanced subsidies expire, a 60-year-old Michigan couple earning $82,000 (just above 400% FPL for two) could see their premium jump from approximately $580/month to over $1,900/month — a $15,800/year increase. Michiganders near the cliff should carefully model their projected income with an enrollment assistant. Small adjustments (HSA contributions, deductible IRA contributions) can keep MAGI below the threshold and preserve thousands in subsidies.

Healthy Michigan Plan and Medicaid

Healthy Michigan Plan is Michigan’s Medicaid expansion program covering adults ages 19–64 with household income up to 133% of the Federal Poverty Level — roughly $20,783 for a single adult or $42,760 for a family of four in 2026. Approximately 2.4 million Michiganders are enrolled in Medicaid and Healthy Michigan Plan combined, making it the largest source of health coverage in the state after employer-sponsored insurance. Coverage is comprehensive, with low copays and no monthly premium for most enrollees.

Michigan’s Medicaid unwinding process — which resumed in 2023 after the pandemic-era continuous coverage rule ended — shifted approximately 160,114 Michiganders from Medicaid to Marketplace coverage through early 2025. These transitions contributed to Michigan’s record-high marketplace enrollment in 2024 and 2025 before the 2026 carrier exits and subsidy uncertainty. Healthy Michigan Plan enrollees who lose eligibility due to income changes can enroll in a HealthCare.gov plan through a Special Enrollment Period triggered by loss of Medicaid coverage.

Applying for Healthy Michigan Plan happens through the Michigan Department of Health and Human Services — not through HealthCare.gov, though HealthCare.gov screens eligibility and routes applicants to MDHHS when appropriate. Medicaid and Healthy Michigan Plan allow year-round enrollment regardless of the Marketplace Open Enrollment Period. The affordable coverage guide details when Healthy Michigan Plan is a better fit than a subsidized Marketplace plan.

Michigan Health Insurance by Region

Michigan health insurance options vary significantly by region. Detroit metro residents have the most carrier options with access to BCBS, Blue Care Network, Meridian, Oscar, and UnitedHealthcare. West Michigan (Kent, Ottawa, Kalamazoo counties) is Priority Health territory. Central Michigan near Flint has McLaren Health Plan as a local specialty option. The Upper Peninsula has the fewest choices — typically only BCBS and Blue Care Network statewide carriers reach rural northern counties.

Detroit metro — Wayne, Oakland, Macomb, and Washtenaw counties — is Michigan’s most competitive insurance market. The largest health systems operate here: Henry Ford Health, Beaumont (now Corewell Health East), Detroit Medical Center, University of Michigan Health (Ann Arbor), and St. Joseph Mercy. All seven marketplace carriers maintain networks in at least part of the metro, and the competition keeps premiums lower than many rural regions. Detroit’s significant Black population and Dearborn’s large Arab American community both benefit from carriers that contract with the community health centers serving these populations.

West Michigan is Priority Health’s home market, competing with BCBS and Blue Care Network. Priority’s integration with Corewell Health (formerly Spectrum Health) gives it a structural advantage in Kent, Ottawa, Muskegon, and Kalamazoo counties. The Flint area relies heavily on McLaren Health Plan, which operates as the insurance arm of the McLaren Health Care hospital system. Lansing-area residents lost a major carrier when UM Health Plan (Physicians Health Plan) dissolved — those 64,000 enrollees needed to switch to BCBS, Blue Care Network, or Priority Health for 2026. The best carriers guide covers regional network strength in detail.

Short-Term Health Insurance in Michigan

Short-term health insurance is available in Michigan as a temporary stopgap — for example, between jobs or while waiting for marketplace coverage to begin. Michigan permits short-term plans, but federal rules now cap them at three months of initial coverage with a maximum of four months total including renewals. These plans are not ACA-compliant: they can deny coverage for pre-existing conditions, exclude essential benefits, and impose dollar caps, so they are rarely the best long-term choice for Michigan residents.

For most Michiganders, a subsidized marketplace plan is both more comprehensive and often cheaper than a short-term policy once premium tax credits are applied. Short-term coverage makes sense in narrow situations: a brief gap before employer coverage starts, or a missed Open Enrollment window with no Qualifying Life Event. Even then, a Special Enrollment Period or Healthy Michigan Plan eligibility is worth checking first, because either can provide real ACA coverage that short-term plans cannot match. Anyone considering a short-term plan should compare it against a subsidized marketplace option before enrolling.

How to Enroll in Michigan Health Insurance for 2026

Enrolling in a Michigan marketplace plan happens through HealthCare.gov, the federal exchange. Open Enrollment for 2026 coverage ran November 1, 2025 through January 15, 2026. Outside Open Enrollment, Michiganders need a Qualifying Life Event — marriage, birth, job loss, loss of Medicaid, moving to Michigan — to trigger a 60-day Special Enrollment Period. Healthy Michigan Plan and Medicaid allow year-round enrollment through the Michigan Department of Health and Human Services.

For 2027 coverage, the federal government shortened Open Enrollment to November 1 through December 15, 2026 — six weeks instead of the previous ten-week window. All plans selected during that window will take effect January 1, 2027. There is no automatic renewal for 2026 enrollees; every household must actively select and confirm a plan, update income and household information, and confirm subsidy eligibility. Missing the December 15 deadline without a Qualifying Life Event means going uninsured until the following year’s Open Enrollment. The Michigan marketplace guide walks through the enrollment process step by step.

Frequently Asked Questions About Michigan Health Insurance

How much does Michigan health insurance cost in 2026?

Michigan health insurance premiums increased an average of 20.1% for 2026. A 40-year-old in Wayne County pays approximately $486/month for a Silver plan before subsidies. After premium tax credits, 90% of Michigan marketplace enrollees pay significantly less — the average after-subsidy cost is approximately $106/month. Costs vary by county, age, tobacco use, and carrier selection.

Which carriers offer Michigan health insurance for 2026?

Seven carriers offer individual plans on HealthCare.gov for Michigan in 2026: Blue Cross Blue Shield of Michigan, Blue Care Network of Michigan, Priority Health, Meridian Health Plan (Ambetter), McLaren Health Plan, Oscar Health, and UnitedHealthcare Community Plan. This is down from ten carriers in 2025, following exits by Molina Healthcare, HAP CareSource, and the University of Michigan’s UM Health Plan.

What happens if my 2025 Michigan health insurance carrier exited?

Former enrollees of Molina Healthcare, HAP CareSource, or UM Health Plan needed to actively select a new carrier on HealthCare.gov for 2026. There was no automatic transfer to a different plan. If you missed Open Enrollment, you generally cannot enroll in a marketplace plan without a Qualifying Life Event (such as marriage, birth, or loss of other coverage). Healthy Michigan Plan and Medicaid enrollment remains available year-round.

Who qualifies for Healthy Michigan Plan?

Healthy Michigan Plan is Michigan’s Medicaid expansion program for adults ages 19–64 with household income up to 133% of the Federal Poverty Level — approximately $20,783 for a single adult or $42,760 for a family of four in 2026. Coverage is comprehensive with low copays and no monthly premium for most enrollees. Apply through the Michigan Department of Health and Human Services; year-round enrollment is available regardless of the Marketplace Open Enrollment Period.

Why did Michigan health insurance rates increase so much in 2026?

Michigan’s 20.1% average rate increase reflects multiple factors: the expiration of enhanced Premium Tax Credits from the American Rescue Plan and Inflation Reduction Act, the departure of three carriers from the individual market, continued medical cost inflation, prescription drug price increases, and a BCBS of Michigan 2024 underwriting loss of $1.7 billion. Uncertainty over whether Congress will extend enhanced subsidies contributed significantly to carrier pricing decisions.

When does Michigan Open Enrollment end?

Open Enrollment for 2026 coverage ran November 1, 2025 through January 15, 2026. For 2027 coverage, the federal government shortened the window to November 1 through December 15, 2026 — six weeks instead of ten. All plans selected during that window take effect January 1, 2027. Outside Open Enrollment, a Qualifying Life Event is required to enroll.

Can I keep my doctor with Michigan marketplace plans?

Keeping your current doctor depends on whether that provider is in your new plan’s network. Blue Cross Blue Shield of Michigan offers the broadest statewide PPO network and the highest likelihood your current doctors are in-network. Blue Care Network (BCBS’s HMO affiliate) has a narrower but still substantial network. Priority Health dominates west Michigan. Always verify your specific providers in each carrier’s directory before enrolling.

Michigan Health Insurance Resources

Explore related guides for Michigan marketplace enrollment, top carrier comparisons, small business and group plans, and PPO options to help navigate health insurance decisions across the Great Lakes State.

How to enroll on HealthCare.gov, deadlines, and qualifying life events.

Top Carriers & PPO PlansBCBSM, Priority Health, and Meridian ranked and compared.

Small Business & Group PlansSHOP, ICHRA, and group coverage options for Michigan employers.

PPO Health Insurance PlansNationwide out-of-network flexibility for specialists and travel.

Compare 2026 Michigan Health Insurance Plans

See all seven Michigan marketplace carriers, check Healthy Michigan Plan eligibility, and get after-subsidy pricing from a licensed enrollment assistant. Free, no cost to you.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Michigan residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.