Individual Health Insurance Indiana 2026: Plans & Costs Guide

Indiana residents purchasing individual health insurance Indiana options in 2026 can choose from marketplace plans on HealthCare.gov, off-exchange private plans, or Medicaid through HIP 2.0, depending on income and coverage needs. This guide covers individual health insurance options in Indiana for the self-employed, freelancers, those between jobs, and anyone not covered by an employer plan.

What brings you here today?

Individual Health Insurance Indiana: Coverage Options

Indiana residents buying individual health insurance in 2026 have three main paths: the federal marketplace (HealthCare.gov, five carriers, subsidy-eligible), off-exchange private plans (Anthem PPO direct, no subsidies), and HIP 2.0 Medicaid (for those earning under $22,026/year single). Over 359,000 Hoosiers enrolled in marketplace plans during 2025 open enrollment per CMS’s 2026 Marketplace Snapshot, with about 80% receiving premium tax credits.

Bronze: Lowest Premium

Age 40, Indianapolis, before subsidies. High deductible ($6,000–$8,500). Best for healthy, low-care-use individuals.

Silver: Benchmark Tier

Age 40, Indianapolis, before subsidies. Qualifies for cost-sharing reductions at 100–250% FPL. Most popular tier.

Gold: Lower Deductible

Age 40, Indianapolis. Higher premium but deductibles as low as $500–$1,500. Best for regular care users.

Off-Exchange PPO Silver

Anthem direct, age 40, Indianapolis. Not subsidy-eligible but no CSR loading, often cheaper than on-exchange Silver for higher earners.

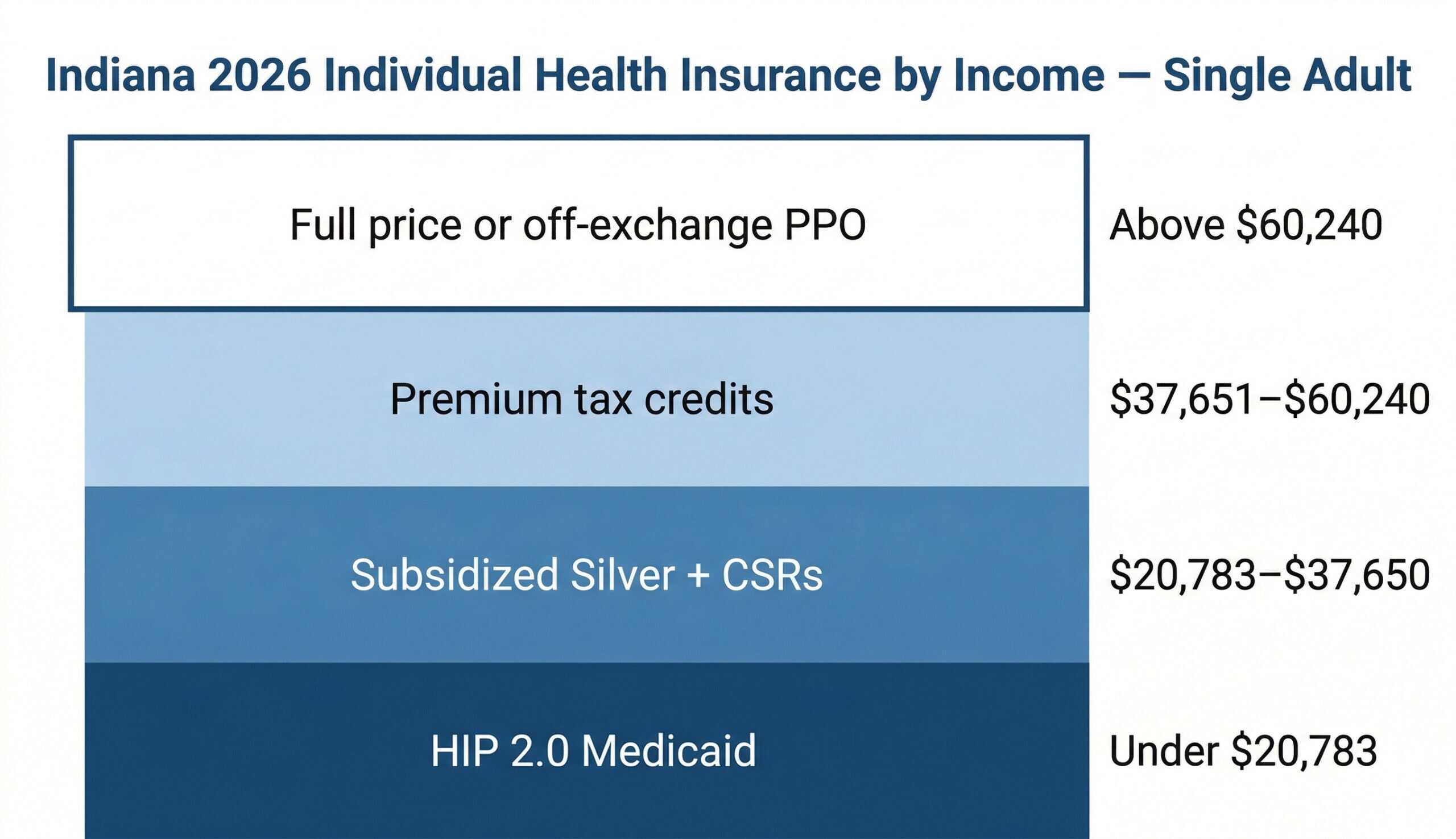

Individual Health Insurance Indiana by Income Level

Income determines which type of individual health insurance Indiana residents should consider first. Hoosiers under $22,026/year (single, 138% FPL) should apply for HIP 2.0 through Indiana FSSA. Those earning $22,026–$62,600 qualify for premium tax credits on the marketplace. Above $62,600, off-exchange Anthem PPO Silver plans often cost $30–$60/month less than on-exchange Silver due to the elimination of cost-sharing reduction premium loading.

Under $22,026/year: HIP 2.0

Apply through Indiana FSSA’s HIP 2.0 program page, not HealthCare.gov. HIP 2.0 requires monthly POWER account contributions ($1–$27/month) for HIP Plus benefits including dental and vision. Enrollment is open year-round, no open enrollment window required.

$22,026–$39,125: Silver + CSRs

The highest-value zone for individual health insurance in Indiana. Cost-sharing reductions on Silver plans reduce deductibles from ~$4,000 to as low as $800, while premium tax credits reduce monthly premiums. This combination of benefits is not available on any other metal tier.

$39,126–$62,600: Subsidized Marketplace

Premium tax credits reduce costs across Bronze, Silver, and Gold tiers. Credits phase out as income rises toward 400% FPL. At $50,000/year for a single adult (~320% FPL), estimated net Silver premium is approximately $200–$280/month depending on county and carrier.

Above $62,600: Off-Exchange or Full-Price

Limited or no premium tax credits in 2026 after the enhanced subsidies expired. Comparing on-exchange Silver against off-exchange Anthem PPO Silver plans is critical at this income level. Off-exchange Silver at $430–$460/month often beats on-exchange Silver for non-subsidy-eligible Hoosiers who value PPO flexibility.

Individual Health Insurance for Self-Employed Indiana Residents

Self-employed Hoosiers (freelancers, independent contractors, 1099 workers, and sole proprietors) can deduct 100% of health insurance premiums as a business expense under IRS rules, reducing the effective cost of individual coverage. For a self-employed Indiana resident paying $490/month for a Silver plan in Indianapolis, that’s a potential $5,880/year deduction. Self-employed residents earning above $62,600 who want broad provider access typically favor Anthem off-exchange PPO plans for direct specialist access at IU Health, Franciscan, and Parkview without referrals.

Indiana has no state-level requirement for self-employed health insurance beyond the federal ACA framework. The self-employed premium deduction (IRS Form 7206) is taken on Schedule 1 of Form 1040, not as a business deduction on Schedule C. The deduction cannot exceed net self-employment income for the year. A self-employed Hoosier earning $62,600 or less (400% FPL single) may also qualify for marketplace premium tax credits through HealthCare.gov, while those earning under $22,026 qualify for HIP 2.0 administered by Indiana FSSA instead. Farm operators and independent contractors across Indiana’s agricultural, construction, and service sectors commonly combine the federal self-employed deduction with either marketplace subsidies or off-exchange Anthem PPO plans, depending on income. For detailed IRS rules on the self-employed deduction, see IRS Form 7206 guidance.

Example: Carmel, Indiana freelance designer, age 38, income $72,000

At approximately 460% FPL (above the primary subsidy threshold), this Hoosier won’t receive premium tax credits on HealthCare.gov. An on-exchange Silver plan might run $460–$510/month. An off-exchange Anthem Silver PPO plan would run approximately $440–$460/month while providing direct specialist access at IU Health North (Carmel) and Ascension St. Vincent without referrals. The 100% self-employed premium deduction reduces the effective after-tax cost by roughly 22–24% depending on marginal tax rate.

Compare Individual Health Insurance Plans in Indiana

Marketplace, off-exchange PPO, and HIP 2.0 options for Indiana individuals. Free quote, no obligation.

Individual Health Insurance Indiana: COBRA vs Marketplace

Indiana residents who lose job-based coverage have 60 days to elect COBRA continuation or enroll in an individual marketplace plan through a Special Enrollment Period. COBRA maintains the employer plan and network but typically costs 102% of the full premium, often $500–$800/month for single coverage. A comparable marketplace Silver plan in Indiana runs $200–$350/month after subsidies for many Hoosiers, making COBRA the more expensive choice in most cases.

| Factor | COBRA (Indiana) | Marketplace Plan (Indiana) |

|---|---|---|

| Monthly cost | 102% of full employer premium, typically $500–$800/mo single | Varies; subsidies available; $200–$490/mo depending on income |

| Subsidy eligibility | None, full premium always | Premium tax credits for incomes 100%–400% FPL |

| Network | Stays on same employer plan network | New carrier network; verify providers before enrolling |

| Coverage start | Retroactive, backdates to job loss | First of following month (after Dec 15 deadline) |

| Duration | Up to 18 months (36 for disability) | Ongoing, no expiration if premiums paid |

| Best for | Active health treatment where continuity matters | Most Hoosiers eligible for subsidies; lower-cost option |

COBRA and Marketplace Enrollment Don’t Overlap

Electing COBRA does not disqualify Indiana residents from later switching to a marketplace plan. When COBRA expires (or if COBRA is voluntarily dropped), a new 60-day SEP opens to enroll in marketplace coverage. However, voluntarily dropping COBRA mid-year is not a qualifying life event, so plan the transition carefully.

Qualifying Life Events for Individual Health Insurance Indiana

Outside of open enrollment (November 1 – January 15), individual health insurance Indiana enrollment is available only through a Special Enrollment Period triggered by a qualifying life event. Common Indiana QLEs include losing job-based coverage, moving to Indiana, getting married, having a child, or losing HIP 2.0 eligibility when income rises above 138% FPL. Each QLE opens a 60-day enrollment window on HealthCare.gov.

- Lost employer coverage (most common): job loss, layoff, hours reduction, or end of employer eligibility

- Lost HIP 2.0 eligibility: Indiana-specific; occurs when income rises above ~$22,026/year single; triggers a 60-day marketplace SEP

- Moved to Indiana from another state or between Indiana counties with different plan availability

- Got married or divorced: marriage adds an SEP; divorce may create a loss-of-coverage SEP

- Had or adopted a child: newborns can be enrolled retroactively to date of birth within 60 days

- Aged off a parent’s plan: turning 26 triggers a 60-day SEP regardless of open enrollment timing

- COBRA expiration: when COBRA exhausts (18 months), a new 60-day SEP opens

Frequently Asked Questions About Individual Health Insurance in Indiana

Common questions Hoosiers ask about individual health insurance in 2026: cheapest plan options (Bronze averages ~$340/month before subsidies), HIP 2.0 eligibility at $22,026 single income, subsidy thresholds up to $62,600 (400% FPL), the five Indiana marketplace carriers (Anthem, Ambetter, CareSource, Cigna, UnitedHealthcare), self-employed premium deductions on IRS Form 7206, and enrolling outside the Nov 1–Jan 15 open enrollment window.

What is the cheapest individual health insurance in Indiana for 2026?

The cheapest individual health insurance in Indiana depends on income. Hoosiers earning under $22,026/year (single) can get HIP 2.0 Medicaid at minimal or no cost through Indiana FSSA. For those on the marketplace, a Bronze plan averages ~$340/month before subsidies. With credits applied, many Hoosiers pay well under full price. At higher incomes without subsidies, Ambetter and CareSource HMO Bronze plans are typically the lowest-premium ACA-compliant options available.

Can self-employed residents get individual health insurance in Indiana?

Yes. Self-employed Hoosiers (freelancers, 1099 contractors, sole proprietors) purchase individual health insurance through HealthCare.gov or directly through carriers like Anthem for off-exchange plans. Self-employed residents can also deduct 100% of health insurance premiums as a business expense under IRS rules (Form 7206), reducing the effective cost of coverage. The deduction is taken on Schedule 1 of Form 1040, not on Schedule C.

What is the income limit for individual health insurance subsidies in Indiana?

For 2026, premium tax credits are available to Indiana individuals earning between 100% and 400% of the Federal Poverty Level, roughly $15,650 to $62,600 for a single adult. The enhanced credits that previously extended eligibility above 400% FPL expired at the end of 2025, so Hoosiers earning above $62,600 in 2026 generally receive no premium tax credit. The $15,650 single-person FPL used for 2026 marketplace subsidies comes from ASPE’s 2025 Poverty Guidelines. Hoosiers under $22,026/year (138% FPL) qualify for HIP 2.0 instead of marketplace plans.

Is COBRA or marketplace coverage better for Indiana residents?

For most Indiana residents who qualify for marketplace subsidies, a marketplace Silver plan costs significantly less than COBRA, often $200–$350/month after credits versus $500–$800/month for COBRA. COBRA is worth considering only if active treatment is underway and network continuity matters, or if income is too high to qualify for subsidies and the employer plan’s network is important to maintain. COBRA lasts up to 18 months; marketplace plans continue indefinitely with premium payments.

What individual health insurance options are available if I missed open enrollment in Indiana?

Missing open enrollment (which ends January 15) doesn’t leave Indiana residents without options. A qualifying life event triggers a 60-day Special Enrollment Period on HealthCare.gov; common QLEs include losing other coverage, getting married, having a child, or moving to Indiana. Indiana also allows short-term health insurance plans (up to 364 days under federal rules) as a stopgap. HIP 2.0 enrollment is open year-round for eligible Hoosiers.

More Indiana Health Insurance Resources

Complete overview of coverage options for Hoosiers, including carriers, costs, HIP 2.0, and enrollment.

Indiana Marketplace & EnrollmentHealthCare.gov enrollment, subsidy eligibility, and open enrollment dates for Indiana residents.

Best Health Insurance in IndianaCompare top carriers in Indiana by cost and network: Anthem, Ambetter, CareSource, Cigna, and UnitedHealthcare.

Indiana Health Insurance BrokersHow licensed Indiana brokers help with plan comparison and enrollment at no cost to Hoosiers.

Affordable Health Insurance in IndianaHow to lower your Indiana health insurance costs with subsidies, HIP 2.0, and off-exchange comparisons.

Indiana Short-Term Health InsuranceShort-term coverage options in Indiana for gaps between jobs or SEP windows, plus what they cover and limits.

Indiana Small Business Health InsuranceGroup coverage for Indiana businesses with 1–50 employees: SHOP marketplace, carriers, and tax credits.

PPO vs HMO vs EPO vs POSNational comparison of plan types with network rules, referrals, and costs explained for Indiana shoppers.

PPO Health Insurance PlansNational PPO plan hub covering how PPO networks, referrals, and out-of-network benefits work.

Get Indiana Individual Health Insurance Quotes for 2026

Marketplace Silver plans from ~$137/month after subsidies (~359,000 Hoosiers enrolled in 2025, 80% receiving an average credit of $481/month), off-exchange Anthem PPO options for income above $62,600 (400% FPL), and HIP 2.0 at $0 for adults earning up to $22,026 — compare all Indiana options and find your coverage.

Get a Quote Call 888-215-4045Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Indiana residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.