Kentucky Health Insurance: 2026 Plans, Costs & Enrollment Guide

Kentucky residents have several paths to health coverage in 2026 — from kynect marketplace plans and Medicaid to off-exchange PPO options for those who don’t qualify for subsidies. This guide covers the carriers available in Kentucky this year, what plans cost after the 2026 subsidy changes, and how to find coverage that fits your situation.

What brings you here today?

How Kentucky Health Insurance Works in 2026

Kentucky runs its own state-based exchange — kynect — one of roughly 18 states that operate independently from HealthCare.gov. In 2026, approximately 89,000 Kentuckians enrolled through kynect, down from 97,000 in 2025 after the expiration of enhanced federal subsidies. Three carriers offer individual marketplace plans in 2026, down from four after CareSource exited. Kentucky has no state individual mandate penalty.

Kentuckians shop for marketplace coverage at kynect.ky.gov — not HealthCare.gov. This is a distinction that matters: kynect has its own enrollment platform and a network of state-certified enrollment assisters called “kynectors” — though licensed agents can access both kynect plans and off-exchange options that kynectors cannot show.

Kentucky’s exchange has an unusual history. Governor Steve Beshear launched kynect in 2013 as one of the most successful state exchanges in the country. His successor, Matt Bevin, shut it down in 2017 and moved Kentuckians to HealthCare.gov. Governor Andy Beshear then relaunched kynect in 2022 — making Kentucky the only state to have deactivated and restarted its own exchange. That history matters because it means some Kentuckians still associate the marketplace with HealthCare.gov, even though kynect has been fully operational since the 2022 plan year.

No state mandate in Kentucky: Unlike California ($900+/adult penalty) or New Jersey, Kentucky does not charge a state tax penalty for being uninsured. The federal penalty was eliminated after 2018. However, going without coverage carries real financial risk — a single hospitalization in Louisville or Lexington can exceed $30,000 without insurance.

How Much Does Health Insurance Cost in Kentucky?

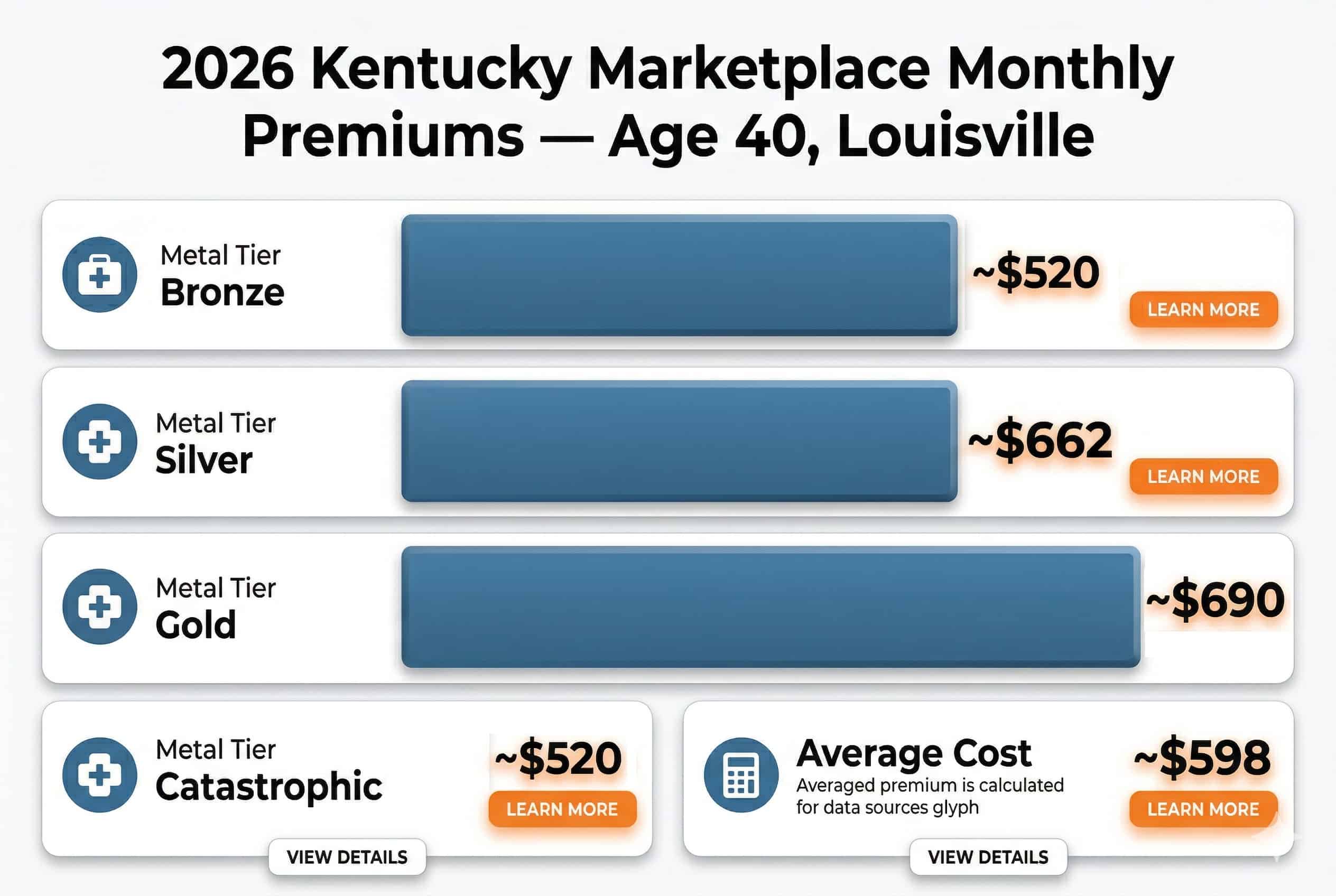

Kentucky marketplace premiums for a 40-year-old average roughly $662/month for a Silver plan and approximately $520/month for a Bronze plan in 2026, before subsidies. These represent significant increases from 2025 — premium hikes of 15%–37% across carriers — driven by both base rate increases and the expiration of enhanced federal subsidies at the end of 2025. Subsidized enrollees are seeing out-of-pocket cost increases averaging $181–$200/month.

Bronze Plan

~$520/mo

Age 40, Louisville. Lowest premiums, highest out-of-pocket costs. Deductibles typically $7,850–$10,600. HSA-eligible options available.

Silver Plan

~$662/mo

Age 40, statewide average. Benchmark tier for subsidy calculations. Cost-sharing reductions available for incomes up to 250% FPL — 48% of 2025 enrollees selected Silver CSR plans.

Gold Plan

~$690/mo

Age 40, Louisville. Higher premiums, lower deductibles (~$1,125–$2,300). Worth considering if you use care regularly or take multiple prescriptions.

Catastrophic Plan

~$520/mo

Age 40, Louisville. Available to adults under 30 or those with a hardship exemption. High deductible ($10,600), three free primary care visits per year before deductible.

The 2026 Subsidy Situation in Kentucky

The enhanced premium tax credits created by the Inflation Reduction Act expired at the end of 2025. For Kentucky’s marketplace enrollees, this means two major changes in 2026: subsidies are smaller for those who still qualify, and households earning above 400% of the Federal Poverty Level (~$62,600 for a single adult) are now completely ineligible for subsidies. In 2025, Kentucky enrollees received subsidies averaging $489/month, producing an average net premium of $180/month. In 2026, the average subsidy covers less of the total premium, and net out-of-pocket costs have increased by $181–$200/month for many households.

The impact is particularly acute for older Kentuckians and moderate-income families. A 60-year-old small business owner in Christian County earning $62,700/year — just above the subsidy cutoff — would see monthly premiums increase from approximately $444 to $933 compared to 2025. A family of three in Berea earning $50,000/year would see their net premium rise from $63/month to roughly $250/month.

| Household Income (Single Adult) | % of FPL | Coverage Pathway |

|---|---|---|

| Under $22,025 | Under 138% | Kentucky Medicaid (year-round enrollment via kynect) |

| $22,025 – $31,200 | 138–200% | Subsidized kynect marketplace (strong credits + CSR) |

| $31,201 – $47,000 | 200–300% | Subsidized kynect marketplace (moderate credits) |

| $47,001 – $62,600 | 300–400% | Subsidized kynect marketplace (smaller credits) |

| Over $62,600 | Above 400% | Full-price kynect or off-exchange coverage |

Kentucky residents above the subsidy threshold often find that off-exchange plans from Anthem — purchased directly rather than through kynect — run slightly less than equivalent on-exchange Silver plans, because off-exchange plans don’t carry cost-sharing reduction loading. See Kentucky PPO and off-exchange plan options for current Anthem pricing.

Kentucky Medicaid — Expansion, HB 2, and What’s Changing

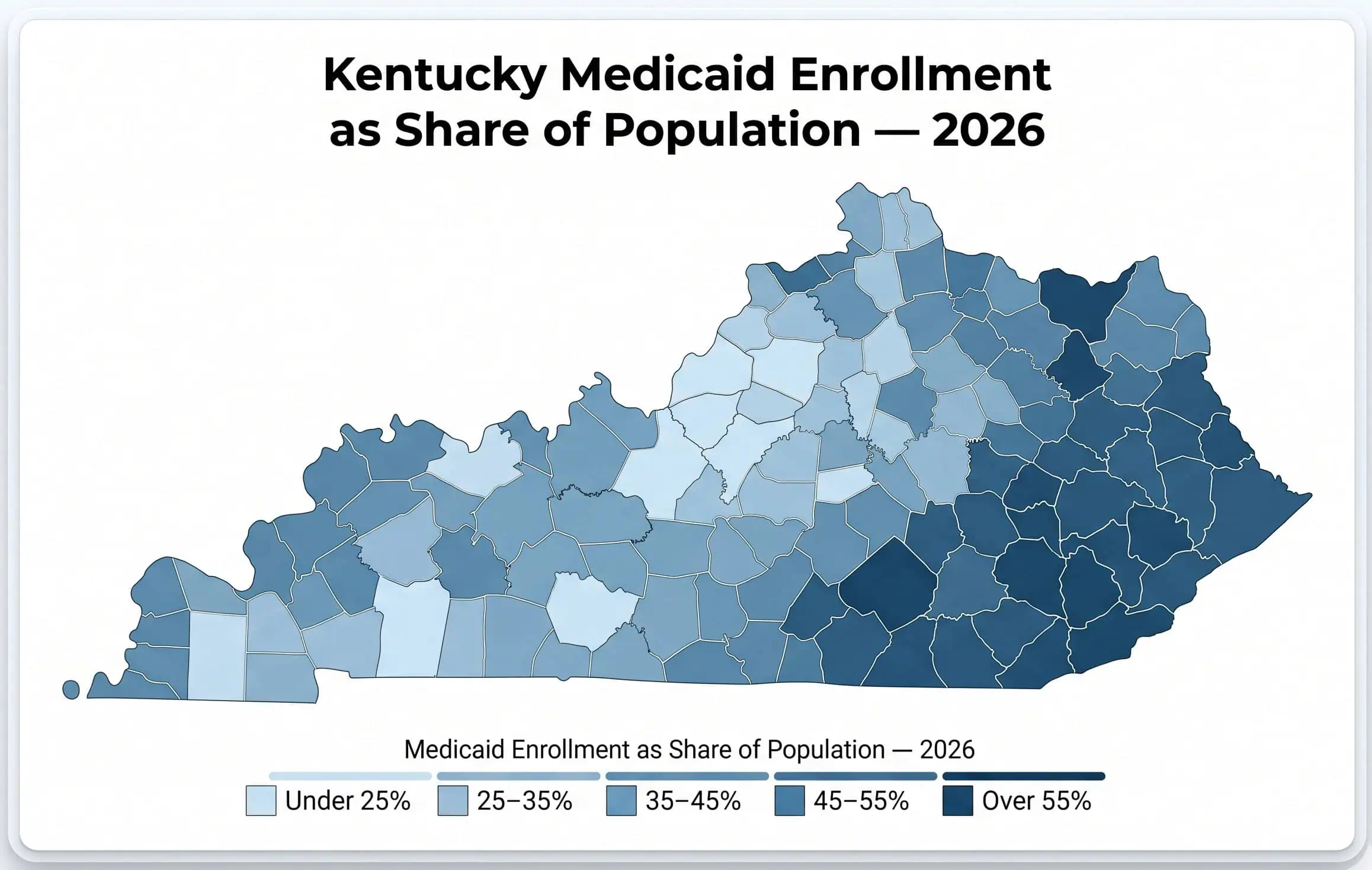

Kentucky expanded Medicaid in 2014 under Governor Steve Beshear, reducing the state’s uninsured rate from 14.3% to 5.4% — one of the largest drops in the country. Approximately 1.5 million Kentuckians are currently enrolled in Medicaid, including roughly 478,900 adults covered through the ACA expansion. In April 2026, Kentucky enacted HB 2, which introduces $5 copays for most Medicaid services, $1 copays for prescription drugs, and community engagement requirements for expansion enrollees.

Kentucky Medicaid covers adults ages 19–64 earning up to 138% of the Federal Poverty Level — approximately $22,025/year for a single adult in 2026. Children qualify through Medicaid (up to 147% FPL) or the Kentucky Children’s Health Insurance Program, KCHIP (up to 218% FPL, roughly $59,558 for a family of three). Pregnant women qualify with incomes up to 200% FPL ($31,920/year). Enrollment is open year-round through kynect.ky.gov — there is no restricted enrollment window for Medicaid.

Medicaid managed care in Kentucky is delivered through five managed care organizations (MCOs): Aetna Better Health of Kentucky, Humana Healthy Horizons in Kentucky, Passport Health Plan by Molina Healthcare, UnitedHealthcare Community Plan, and WellCare of Kentucky. Enrollees choose an MCO when they sign up, and each MCO has its own provider network across the state. The share of Kentuckians covered by Medicaid varies dramatically by county — from 17.9% in Spencer County to 68.8% in Owsley County in eastern Kentucky.

HB 2 — Kentucky Medicaid Reform (2026): House Bill 2 was passed by the Kentucky General Assembly in April 2026. The original House version called for $35 copays on inpatient hospital services and $8 copays on prescription glasses; the Senate amended these down to $5 copays on most healthcare services and $1 copays on prescription drugs. The final law caps total copays at 5% of family income and adds community engagement/work verification requirements for approximately 478,900 expansion adults. Kentucky becomes one of the first states to implement Medicaid copays and work requirements under the One Big Beautiful Bill Act framework.

Kentucky Health Insurance Carriers in 2026

Kentucky’s kynect marketplace has 3 carriers for 2026 — down from 4 after CareSource exited at the end of 2025. The remaining carriers are Anthem Blue Cross Blue Shield (Pathway HMO and Transition HMO networks), Ambetter by WellCare of Kentucky (Centene-owned, 108 of 120 counties), and Passport Health Plan by Molina Healthcare (5 Bluegrass-region counties). Kentucky’s 2026 rate increases ranged from 15.1% to 37% — more than 10 times recent-year increases.

Anthem Blue Cross Blue Shield

- Two network tiers: Pathway HMO (narrower, lower cost) and Transition HMO (broader network)

- Only carrier serving all 120 Kentucky counties — and only one with off-exchange options

- Broadest provider network — includes Baptist Health, Norton Healthcare, UK HealthCare

- Silver plans ~$714/month (age 40); Bronze ~$547/month

- Gold plans available with $2,300 deductibles

Ambetter by WellCare of Kentucky

- Centene Corporation subsidiary — underwritten by WellCare Health Plans of Kentucky, Inc.

- Available in 108 of Kentucky’s 120 counties for 2026

- Most affordable Silver plans in Kentucky (~$617/month, age 40)

- Gold plans at ~$687/month with $1,125 deductibles

- HMO/EPO network-based plans; WellCare also operates as a Kentucky Medicaid MCO

Passport Health Plan by Molina Healthcare

- Available in 5 Bluegrass-region counties: Clark, Fayette, Jessamine, Scott, and Woodford

- Strong presence in Lexington and central Kentucky

- HMO network plans through the kynect marketplace

- Molina also operates Passport as a Kentucky Medicaid MCO

- Re-entered the Kentucky individual market through the kynect 2022 relaunch

CareSource, which had served Kentucky’s marketplace since its expansion into the state, stopped offering individual market plans at the end of 2025. This means rural eastern Kentucky counties — where carrier choice was already limited — may now have only one or two carriers available. Kentuckians in counties with limited carrier options can use kynect’s county-level plan finder or call a licensed enrollment assistant to compare what is available in their area.

Carrier rate increases for 2026: Before the One Big Beautiful Bill Act (OBBBA), Kentucky carrier rate increases for 2026 ranged from 9.9%–24%. After OBBBA passed and the enhanced subsidies expired, carriers revised their rate filings upward to 15.1%–37% — reflecting the expected loss of younger, healthier enrollees who would drop coverage due to higher out-of-pocket costs.

Plan Types: HMO, PPO, and Off-Exchange in Kentucky

Most Kentucky kynect carriers offer HMO or EPO plans — Ambetter by WellCare and Passport by Molina sell network-based plans starting around $617/month for Silver (age 40). Anthem is the only individual-market carrier offering broader network access through its Pathway HMO and Transition HMO tiers, with Transition plans providing access to Baptist Health, Norton Healthcare, and UK HealthCare facilities at Silver premiums of approximately $714/month.

HMO

Referrals required. Must use in-network providers. Lower premiums. Ambetter by WellCare and Passport by Molina offer HMO plans through kynect — Ambetter’s Silver HMO starts around $617/month (age 40).

Anthem Pathway

Narrower Anthem network. Lower Anthem premiums but limited to the Pathway provider list. Good for cost-conscious Kentuckians who confirm their doctors are in the Pathway tier before enrolling.

Anthem Transition / Off-Exchange

Broader network, no referrals. Includes Baptist Health, Norton, UK HealthCare. Silver ~$714/month. Off-exchange options available for those above the subsidy threshold. See Kentucky PPO plans →

For Kentuckians earning above the subsidy cutoff ($62,600 single adult), Anthem’s off-exchange plans — purchased directly through Anthem rather than kynect — may offer slightly lower premiums because off-exchange Silver plans don’t carry cost-sharing reduction loading. The Best Kentucky health insurance guide covers carrier comparisons, Anthem’s network tiers, and off-exchange pricing.

How to Enroll in Kentucky Health Insurance

Kentucky residents enroll through kynect — the state’s own exchange at kynect.ky.gov — during Open Enrollment, which runs November 1 through January 15. Enrolling by December 15 starts coverage January 1. Approximately 89,000 Kentuckians selected marketplace plans during the 2026 open enrollment period, down from 97,000 in 2025 after subsidy cuts. A qualifying life event opens a 60-day Special Enrollment Period. Medicaid enrollment is open year-round.

Determine whether you qualify for Kentucky Medicaid (under ~$22,025/year single), premium tax credits through kynect (up to ~$62,600), or full-price coverage. Income determines which programs and savings apply.

Kentucky uses kynect, not HealthCare.gov. Licensed agents and kynectors (free, state-certified enrollment assisters) can also show you off-exchange plans from Anthem not visible on the kynect marketplace.

After enrolling through kynect, you’ll receive a member ID card within 2–3 weeks. Confirm your first premium payment is received — coverage does not activate until the first payment clears.

Qualifying Life Events in Kentucky

Outside of open enrollment, a qualifying life event (QLE) opens a 60-day window for Kentucky residents to enroll through kynect or switch plans. Common qualifying events include:

- Losing job-based coverage (including COBRA expiration)

- Moving to Kentucky from another state, or moving between Kentucky counties

- Getting married or divorced

- Having or adopting a child

- Losing eligibility for Kentucky Medicaid (e.g., income rising above 138% FPL)

- Turning 26 and aging off a parent’s plan

2027 enrollment change ahead: Starting with the 2027 plan year, kynect’s open enrollment will end no later than December 31 — enrollment will no longer continue into January. Kentucky will decide whether to end enrollment on December 15 (matching HealthCare.gov states) or extend to December 31. All plans selected during OEP will take effect January 1.

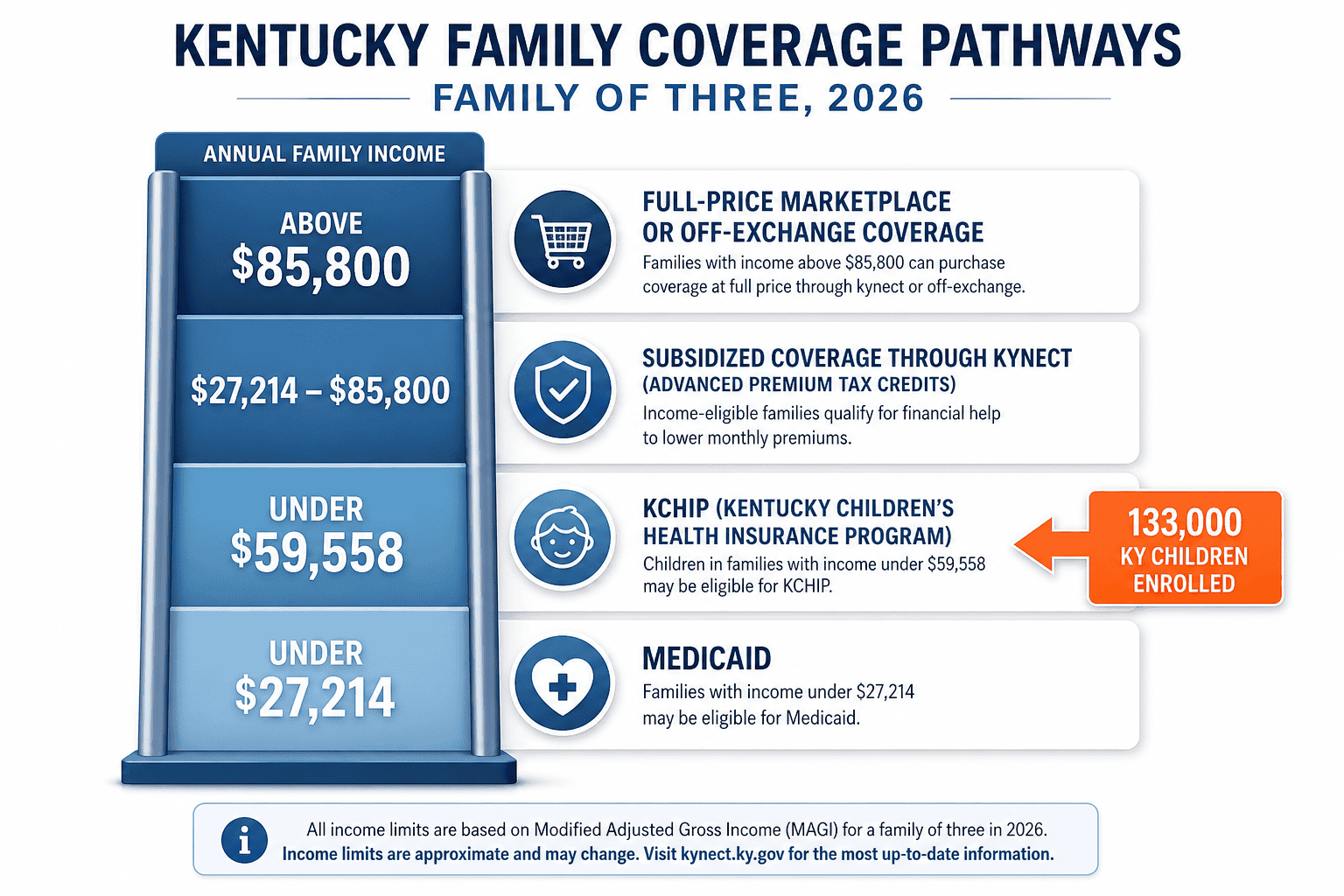

Family and Children’s Coverage in Kentucky

Kentucky families have two main paths to Kentucky health insurance for children: enroll the whole household through kynect marketplace plans, or use KCHIP (Kentucky Children’s Health Insurance Program) for children in households earning up to 218% FPL — roughly $59,558 for a family of three in 2026. KCHIP covers children at low or no cost and includes dental, vision, and preventive services. Approximately 133,000 Kentucky children are enrolled in KCHIP, with another 491,900 children on traditional Medicaid.

For families above the KCHIP threshold, a family Silver plan in Louisville or Lexington can run $1,400–$1,800/month before subsidies, depending on ages and carrier selection. Families with employer offers of coverage that meet ACA affordability standards (less than 9.02% of household income for employee-only coverage) may not qualify for marketplace subsidies, even if their income would otherwise qualify. A licensed enrollment assistant can evaluate whether the employer offer creates an affordability barrier.

Example: Kentucky Family of Three

A family of three in Berea — two parents in their mid-40s and a 14-year-old child — with household income of $50,000 (roughly 213% FPL) would qualify for subsidized kynect Silver coverage. Their estimated 2026 net monthly premium after credits: approximately $250/month, up from roughly $63/month in 2025. The child would also qualify for KCHIP, potentially reducing the family’s coverage costs further by enrolling the child separately.

Short-Term and Gap Coverage in Kentucky

Kentucky allows short-term health insurance plans, but under federal rules effective September 1, 2024, initial terms are limited to 3 months with a maximum total duration of 4 months including renewals — significantly shorter than the 364-day terms previously available. Short-term premiums may run 40–60% less than ACA plans, but these plans can deny pre-existing conditions and exclude essential health benefits. Unlike California and Colorado, Kentucky does not ban short-term plans outright.

The 3-month/4-month limit is a federal change — Kentucky itself did not impose a separate state restriction. After using a short-term plan, Kentucky residents must wait 12 months before purchasing another from the same insurer, and short-term policies are subject to Kentucky Department of Insurance filing review under KRS 304.17A. Kentuckians considering short-term Kentucky health insurance should understand these plans are not ACA-compliant, are not available through kynect, and do not qualify for premium tax credits — meaning a 40-year-old in Lexington paying ~$662/month for a Silver kynect plan after subsidies could pay $200–$300/month short-term but lose protections for pre-existing conditions, mental health, maternity, and prescription drugs. The Kentucky short-term health insurance guide covers current plan options and limitations in detail.

Compare Kentucky Health Insurance Plans

Get quotes side by side from all 3 kynect carriers — Anthem, Ambetter by WellCare of Kentucky, and Passport by Molina — plus off-exchange Anthem options and Kentucky Medicaid eligibility checks at 138% FPL ($22,025/year single). Silver plans average ~$662/month for age 40 before subsidies. No cost, no obligation.

Small Business Health Insurance in Kentucky

Kentucky small businesses with 1–50 full-time employees can offer group coverage through the kynect SHOP marketplace — Anthem Blue Cross Blue Shield is the primary SHOP-certified medical carrier for 2026. Businesses with fewer than 25 FTE averaging under $58,000/year in wages may qualify for the federal Small Business Health Care Tax Credit, worth up to 50% of premiums paid. Kentucky has no state employer mandate.

For Kentucky businesses considering group coverage, the Kentucky small business health insurance guide covers SHOP options through kynect, carrier availability, and tax credit eligibility in detail.

Which Kentucky Plan Is Right for You?

The right Kentucky plan depends on income, health usage, and provider preferences. Residents earning under $22,025 (single) qualify for Kentucky Medicaid, though under HB 2 (enacted April 2026) expansion enrollees pay $5 service copays and $1 prescription copays. Those between $22,025 and $62,600 should start on kynect for subsidy eligibility. Frequent care users often save with Gold plans — deductibles of $1,125–$2,300 versus $7,850–$10,600 on Bronze.

Low income (under 138% FPL)

Apply for Kentucky Medicaid through kynect. Enrollment is open year-round. Five MCOs to choose from: Aetna Better Health, Humana Healthy Horizons, Passport by Molina, UnitedHealthcare Community Plan, and WellCare of Kentucky. Note: HB 2 (enacted April 2026) added $5 service copays and $1 prescription copays for expansion adults, capped at 5% of family income.

Moderate income (138–300% FPL)

Premium tax credits available through kynect. Silver plans with cost-sharing reductions are often the best value at this income level — lower deductibles and out-of-pocket maximums. In 2025, 48% of Kentucky enrollees chose Silver CSR plans.

Higher income (above 400% FPL)

No subsidies available in 2026 (enhanced credits expired). Compare kynect Silver plans against off-exchange Anthem Transition plans — the off-exchange option often costs less without CSR loading.

Self-employed / freelance

Anthem’s broader Transition network allows specialist access at Baptist Health, Norton Healthcare, and UK HealthCare without referrals. Premiums are 100% deductible as a business expense.

Family with children

Check KCHIP eligibility for children first — it covers kids up to 218% FPL at low or no cost. Adults can enroll separately in a kynect marketplace plan. About 133,000 Kentucky children are currently on KCHIP.

Between jobs

Job loss triggers a Special Enrollment Period on kynect. In Kentucky, COBRA costs average ~$702/month for an individual — compare against a subsidized kynect plan, which often costs significantly less.

Frequently Asked Questions About Kentucky Health Insurance

Common Kentucky health insurance questions for 2026 cover the kynect state-based exchange (replacing HealthCare.gov use from 2017–2021), the lack of a state mandate penalty, the 3-carrier kynect lineup after CareSource exited at the end of 2025, the 15.1%–37% rate increases following OBBBA passage, HB 2 Medicaid copays enacted in April 2026, and open enrollment running November 1 through January 15.

Does Kentucky use HealthCare.gov or its own marketplace?

Kentucky uses its own state-based exchange called kynect (kynect.ky.gov) — not HealthCare.gov. Kentuckians shop, compare, and enroll in marketplace plans directly through kynect. The state also uses kynect for Medicaid and KCHIP applications. Kentucky briefly used HealthCare.gov from 2017 to 2021 but relaunched kynect for the 2022 plan year.

Does Kentucky have a penalty for not having health insurance?

No. Kentucky does not have a state individual mandate or tax penalty for being uninsured. The federal penalty was eliminated after 2018. However, going without coverage carries financial risk — a single hospitalization or emergency in Kentucky can result in bills exceeding $30,000 without insurance.

How many carriers are on kynect for 2026?

Three carriers offer individual marketplace plans through kynect for 2026: Anthem Blue Cross Blue Shield (with Pathway HMO and Transition HMO network options, available in all 120 Kentucky counties), Ambetter by WellCare of Kentucky (a Centene subsidiary, available in 108 of 120 counties), and Passport Health Plan by Molina Healthcare (available in 5 Bluegrass-region counties: Clark, Fayette, Jessamine, Scott, and Woodford). This is down from four carriers in 2025 after CareSource exited the Kentucky marketplace. Eleven mostly rural counties — including Fleming, Graves, Grayson, Harrison, Marion, Mason, Montgomery, Pulaski, Robertson, Rowan, and Wayne — have only Anthem available for 2026.

Why did Kentucky health insurance premiums increase so much for 2026?

Two factors drove Kentucky’s 2026 premium increases: base rate hikes of 15.1%–37% across carriers, and the expiration of enhanced federal premium tax credits at the end of 2025. The enhanced subsidies had been keeping out-of-pocket costs low since 2021 — without them, subsidies cover less of the total premium, and households above 400% FPL ($62,600 single adult) lost subsidy eligibility entirely. Enrollees are seeing net cost increases of $181–$200/month on average.

What is HB 2 and how does it affect Kentucky Medicaid?

House Bill 2 is Kentucky legislation enacted by the General Assembly in April 2026 that introduces changes to the Medicaid program. Key provisions include copays for expansion enrollees ($5 for most healthcare services and $1 for prescription drugs in the final Senate-amended version, lowered from the original House version of $35 inpatient hospital and $8 prescription glasses), community engagement and work verification requirements for approximately 478,900 expansion adults, and a cap on total copays at 5% of family income. The law makes Kentucky one of the first states to implement Medicaid copays and work requirements under the One Big Beautiful Bill Act framework.

When is open enrollment for Kentucky health insurance?

Open enrollment for 2026 Kentucky marketplace plans ran November 1 through January 15 on kynect. Enrolling by December 15 started coverage January 1. Starting with the 2027 plan year, open enrollment will end no later than December 31 and will not extend into January. Medicaid and KCHIP enrollment is open year-round. Outside open enrollment, qualifying life events trigger a 60-day Special Enrollment Period on kynect.

Kentucky Health Insurance Resources

kynect enrollment, subsidy eligibility, county carrier availability, and 2026 open enrollment dates

Best Health Insurance in KentuckyCompare all 3 carriers — Anthem, Ambetter by WellCare, Passport by Molina — with Kentucky county coverage

Affordable Health Insurance KentuckyKentucky Medicaid, KCHIP, premium tables, and how HB 2 affects 478,900 expansion adults

Individual Health Insurance KentuckyCoverage for self-employed Kentuckians, Bluegrass farm operators, and residents above the $62,600 subsidy cutoff

Small Business Health Insurance KentuckyGroup plans, kynect SHOP, and ICHRA options for Kentucky’s small business and agricultural employers

PPO Health Insurance PlansCompare PPO options nationwide — flexible provider access, no referrals required, in and out of network

Ready to Find Your Kentucky Health Insurance Plan?

Compare 2026 Kentucky health insurance plans from all 3 kynect carriers — Anthem (~$714 Silver), Ambetter by WellCare (~$617 Silver), and Passport by Molina (5 Bluegrass counties) — plus Kentucky Medicaid for incomes under $22,025, KCHIP for children up to 218% FPL, and off-exchange Anthem options for households above the $62,600 subsidy cutoff. Speak with a licensed enrollment assistant at no cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Kentucky residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.