Health Insurance Broker California: Free Help for 2026

Finding the right health insurance broker California has to offer starts with understanding what brokers do and why the state’s complex market makes professional guidance especially valuable. A licensed agent can compare plans across all 11 Covered California carriers — plus off-exchange PPO options from Blue Shield and Anthem — at no cost to the consumer. California’s individual health insurance market features 19 pricing regions, varying carrier availability by county, a state individual mandate, and significant pricing differences between on-exchange and off-exchange plans. Working with a licensed health insurance professional in California simplifies this process by providing personalized plan comparisons, subsidy calculations, and enrollment assistance without adding any cost to the plan premium.

What Does a Health Insurance Broker Do in California?

A health insurance broker in California is a licensed professional who helps individuals, families, and small businesses compare and enroll in health insurance plans. Licensed agents are credentialed through the California Department of Insurance (CDI) and can access plans from all 11 Covered California carriers as well as off-exchange options — giving them a broader view of the market than any single carrier’s website or call center.

In California, licensed agents provide several specific services that go beyond basic plan selection. They calculate premium tax credit eligibility based on household income and family size, compare on-exchange plans against off-exchange alternatives to determine which option provides better value, navigate the state’s 19 pricing regions where carrier availability and costs vary, and manage enrollment paperwork for both Covered California and direct carrier applications. Enrollment assistance also covers qualifying life events, plan renewals, claims questions, and mid-year coverage changes.

Unlike Covered California navigators or certified enrollment counselors — who can only help with exchange plans — a licensed agent in California can also enroll clients in off-exchange PPO plans from Blue Shield and Anthem Blue Cross that are not available through the exchange. This includes exclusive off-exchange Silver PPO plans that may carry lower premiums for consumers who do not qualify for subsidies. The ability to compare both on-exchange and off-exchange options is particularly valuable in California, where the on/off-exchange pricing gap at the Silver tier is significant.

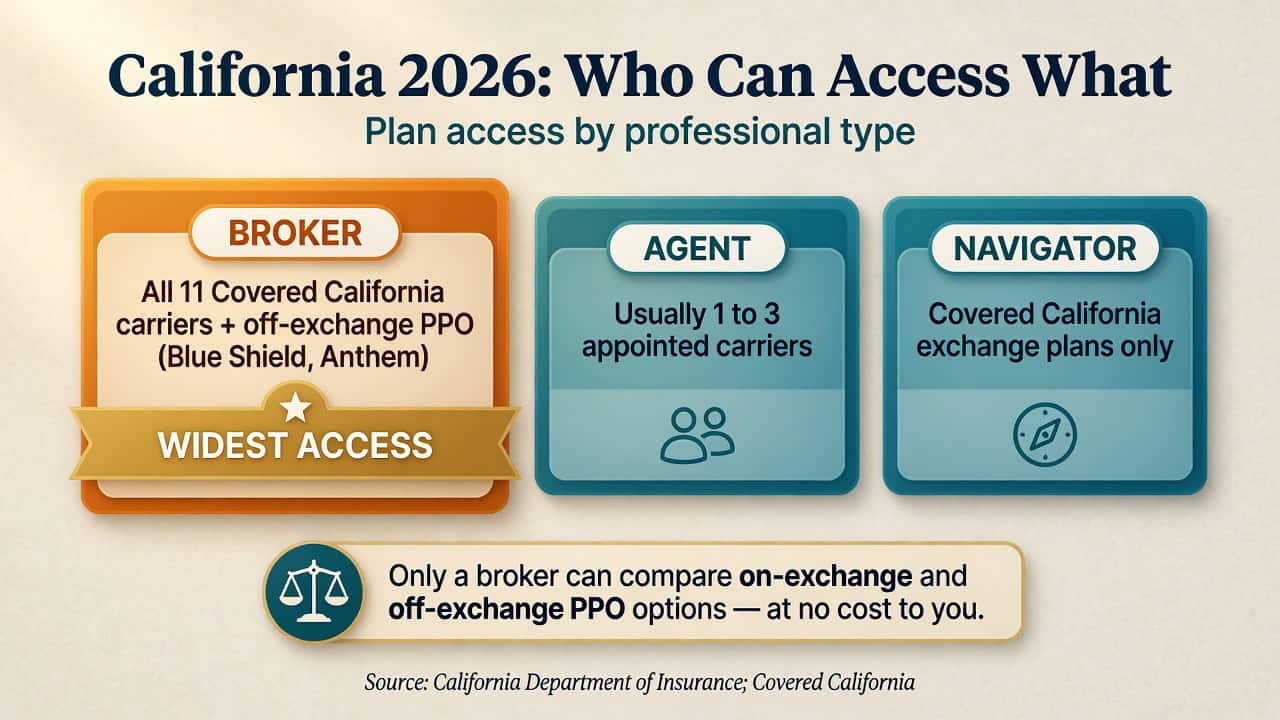

Broker vs. Agent vs. Navigator: Key Differences

California consumers encounter three types of enrollment professionals, each with different capabilities and access levels. Understanding the differences helps residents choose the right type of assistance for their situation, particularly when comparing plans across multiple carriers or evaluating off-exchange PPO options.

| Feature | Insurance Broker | Insurance Agent | Navigator / Counselor |

|---|---|---|---|

| Licensed by CDI? | Yes | Yes | No (certified by Covered CA) |

| Represents multiple carriers? | Yes — all 11 exchange + off-exchange | Usually 1–3 carriers | N/A — facilitates enrollment only |

| Can enroll on Covered California? | Yes | Yes (if Covered CA certified) | Yes |

| Can enroll off-exchange? | Yes | Yes (with appointed carriers) | No |

| Compensation | Carrier commission (no cost to consumer) | Carrier commission | Grant-funded (free) |

| Can compare PPO options? | Yes — on + off-exchange PPOs | Only for appointed carriers | No — exchange plans only |

| Best for | Full-market comparison shopping | Specific carrier expertise | Basic Covered CA enrollment |

Key Distinction

A licensed agent in California can access every carrier and plan available in the state — both on Covered California and off-exchange. This is particularly important for consumers earning above subsidy thresholds, where off-exchange PPO plans from Blue Shield and Anthem may offer better value than on-exchange options.

Why Use a Health Insurance Broker in California?

California’s health insurance market presents more variables than most states, making a health insurance broker California consumers can rely on especially valuable. With 11 exchange carriers, 19 pricing regions, both HMO and PPO options, and meaningful cost differences between on-exchange and off-exchange plans, the number of plan combinations a California resident can choose from often exceeds 100.

11 Carriers, 19 Regions

California’s carrier availability varies by county and pricing region. A plan available in Los Angeles may not exist in Fresno. Licensed agents know which carriers serve each region and can identify options that online tools sometimes miss — particularly off-exchange products not listed on Covered California.

On-Exchange vs. Off-Exchange

Consumers above subsidy thresholds often save money off-exchange, especially on Silver PPO plans that avoid cost-sharing reduction (CSR) loading. A licensed agent in California can run side-by-side comparisons to determine which enrollment channel provides the lower total cost for a given income level.

Subsidy Calculations

Premium tax credit amounts depend on income, family size, and the benchmark Silver plan in each rating region. Licensed agents calculate exact subsidy amounts and can identify situations where a small income change would increase or decrease credit eligibility — helping consumers plan enrollment timing strategically.

Zero Additional Cost

Licensed agents are compensated by insurance carriers through commissions, not by the consumer. Plan premiums are identical whether enrolling directly through Covered California, through a carrier, or through an agent. The comparison, guidance, and enrollment assistance come at no extra charge.

For residents comparing the best health insurance companies in California, enrollment assistance provides a single point of contact who can evaluate all carriers simultaneously rather than requiring separate research on each company’s website.

How Broker Compensation Works in California

Health insurance brokers in California earn commissions paid by the insurance carrier after a consumer enrolls in a plan. This compensation model means any health insurance broker California residents work with charges nothing extra — the plan premium is the same whether purchased directly, through Covered California, or through a licensed agent.

The California Department of Insurance regulates compensation practices. Carriers pay a fixed commission per enrollee, typically on a monthly basis for as long as the consumer remains on the plan. Commission rates are set by each carrier and are generally consistent regardless of which plan or metal tier the consumer selects. This structure reduces — though does not eliminate — financial incentive to recommend one plan over another.

Consumers should feel comfortable asking about compensation and whether the licensed agent is appointed with all available carriers. An agent appointed with all 11 Covered California carriers plus off-exchange options from Blue Shield and Anthem provides the broadest comparison. Those with fewer carrier appointments may not be able to show all available options.

Verification Tip

California residents can verify license status through the CDI Producer License Lookup tool. Confirm that the license is active and includes a Life & Health qualification — this is required to sell health insurance in California. Covered California certification can also be verified through the Covered California Certified Agent directory.

How to Work with a Health Insurance Broker in California

The process of working with a health insurance broker California residents choose follows a structured sequence from information gathering through plan comparison to enrollment. Most consultations complete this process in one or two sessions, though complex situations involving family coverage, self-employment income, or multiple coverage options may require additional discussion.

Share Basic Information

Provide your ZIP code, household size, estimated annual income, ages of all household members, and any preferred doctors or prescription medications. This information determines which carriers and plans are available in your region and what subsidies may apply.

Review Plan Options

The licensed agent presents a comparison of available plans — both on Covered California and off-exchange — showing monthly premiums, deductibles, copays, out-of-pocket maximums, and network details side by side. PPO and HMO options are compared based on your provider preferences.

Evaluate Total Costs

Beyond monthly premiums, the agent helps estimate total annual costs based on expected medical usage. A plan with a lower premium but a $7,000 deductible may cost more overall than a slightly higher premium plan with a $3,000 deductible for someone who uses care regularly.

Enroll and Confirm

Once a plan is selected, the agent handles the enrollment paperwork — whether through Covered California or directly with a carrier — then confirms enrollment, provides plan documents, and remains available for questions about using the plan, filing claims, or making changes.

Worked Example: Los Angeles Freelancer, Age 38, $72,000

David, a 38-year-old freelance photographer in Los Angeles earning $72,000 per year, sought enrollment assistance after spending four hours on Covered California without narrowing down his options. The licensed agent identified that David did not qualify for premium tax credits at his income level, then compared on-exchange Silver HMO plans against an off-exchange Blue Shield Silver 2600 PPO. The PPO carried a $42 lower monthly premium than the comparable on-exchange Silver option — without CSR cost loading — while giving David the flexibility to see any in-network specialist without a referral. Total savings: $504 per year with broader provider access.

A licensed California agent can compare plans across all 11 carriers — both on Covered California and off-exchange — at no cost. Get personalized plan recommendations based on your ZIP code, income, and coverage needs.

What to Look for in a California Health Insurance Broker

Not all licensed agents offer the same level of service or market access. When evaluating any health insurance broker California has available, several factors distinguish someone who can provide comprehensive guidance from one with limited capabilities or carrier access.

The most important factor is carrier appointment breadth. An agent appointed with all 11 Covered California carriers and both off-exchange PPO carriers (Blue Shield and Anthem) can present the full range of options. Those with appointments at only two or three carriers may recommend plans based on availability rather than fit. Ask directly how many carriers are represented and whether enrollment is possible both on Covered California and off-exchange.

Experience with California’s market specifically matters because the state’s 19 rating regions, individual mandate, state-level subsidies, and off-exchange PPO market create dynamics that do not exist in most other states. A licensed agent in California who understands these factors can identify savings opportunities — like the off-exchange Silver PPO pricing advantage — that a general or out-of-state professional may miss.

Licensing verification provides a baseline of professionalism. Active CDI licensing with a Life & Health qualification confirms that the required examinations have been passed and continuing education maintained. The National Association of Insurance Commissioners (NAIC) provides additional guidance on what consumers should expect from licensed insurance professionals. Covered California certification indicates additional training specific to the state exchange. Both credentials can be verified online through the CDI and Covered California directories.

For small business health insurance in California, look for specific experience in group plans and the Covered California for Small Business (SHOP) marketplace — the requirements and carrier options differ substantially from individual coverage.

Frequently Asked Questions About California Health Insurance Brokers

The following questions cover the most common concerns California residents have about working with a licensed agent, including cost, licensing, and what services are provided during enrollment and beyond.

Does a health insurance broker in California cost anything?

No. Any health insurance broker California residents hire is compensated by insurance carriers through commissions — not by the consumer. The plan premium is the same whether enrolling directly through Covered California, through a carrier’s website, or through a licensed agent. The comparison, guidance, and enrollment assistance are included at no extra charge.

Can a broker enroll me in both Covered California and off-exchange plans?

Yes. A licensed agent in California can enroll consumers in on-exchange plans through Covered California (where premium tax credits apply) and in off-exchange plans purchased directly from carriers. This dual access is especially valuable for consumers who earn above subsidy thresholds and may benefit from off-exchange PPO plans with lower Silver-tier premiums.

How do I verify that a California health insurance broker is licensed?

The California Department of Insurance operates a free online Producer License Lookup tool where consumers can search by name or license number. Verify that the license is active with a Life & Health line of authority. For Covered California certification, the exchange’s online directory lists all certified agents who have completed the required marketplace training.

What is the difference between a broker and a Covered California navigator?

Navigators and enrollment counselors are certified by Covered California to help consumers enroll in exchange plans, but they cannot sell off-exchange coverage or represent specific carriers. Licensed agents hold CDI licenses, represent multiple carriers, and can enroll consumers in both on-exchange and off-exchange plans — including PPO options not available through Covered California.

Can a broker help with a qualifying life event enrollment?

Yes. Life events such as losing employer coverage, getting married, having a baby, or moving to a new county can trigger a special enrollment period. A licensed agent in California can verify the qualifying event, help select the right plan based on the changed circumstances, and manage the enrollment within the 60-day window. For residents in coverage gaps, the individual health insurance California guide covers qualifying events and enrollment options in more detail.

Should I use a broker if I already qualify for subsidies?

Subsidy-eligible consumers benefit from enrollment assistance because a licensed agent can calculate the exact credit amount, compare how subsidies apply across different metal tiers, and identify whether a higher-metal plan with smaller out-of-pocket costs might be a better value than a low-premium Bronze plan. The affordable health insurance California guide explains how subsidies work across income levels and plan tiers. These services remain free regardless of whether the consumer qualifies for financial assistance.

Can a broker help my small business choose a group plan?

Yes. Many licensed agents in California also handle group coverage for small businesses. They can compare group plans through Covered California for Small Business (SHOP) and the open market, explain employer mandate rules (applicable to businesses with 50 or more full-time employees), and help navigate ICHRA and QSEHRA reimbursement arrangements as alternatives to traditional group plans.

Related California Health Insurance Resources

Explore the rest of the California coverage library for plan comparisons, cost breakdowns, and enrollment guidance across every stage of the 2026 shopping process.

Complete 2026 guide to coverage options, enrollment, and subsidies.

Best Health Insurance in CaliforniaCarrier comparisons, quality ratings, and network details.

Individual Health InsuranceSelf-employed coverage, mandate details, and plan selection.

Affordable Coverage OptionsCost breakdowns, subsidy strategies, and savings tips.

Talk to a Licensed California Health Insurance Agent

Get free, personalized help comparing plans across all 11 Covered California carriers and off-exchange PPO options. No cost, no obligation, and no pressure to enroll.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving California residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.