Alabama Health Insurance 2026: Plans, Costs and Coverage

This guide covers every way Alabamians get health coverage in 2026 — the federal marketplace, employer plans, Medicaid, and the coverage gap affecting roughly 90,000 residents. Blue Cross Blue Shield of Alabama controls over 90% of the individual market, which simplifies the carrier decision for most people, but 2026 brought the steepest rate increases in years alongside a new fourth carrier. Use this page as your starting point and follow the links to go deeper on each topic.

What are you looking for?

What Changed for 2026 Coverage in Alabama

Alabama marketplace premiums rose 19% to 25% across all carriers for 2026, and the average after-subsidy premium nearly tripled from $44 to $121 per month as enhanced federal subsidies expired. Oscar Insurance entered Alabama as a fourth marketplace carrier, the open enrollment window for 2026 extended to January 15, and starting with 2027 coverage, open enrollment will end December 15 — the extended pandemic deadline is ending.

The premium increases followed the December 31, 2025 expiration of enhanced premium tax credits created by the American Rescue Plan and extended through the Inflation Reduction Act. Those credits had kept average after-subsidy premiums unusually low since 2021. Without them, Alabamians earning between 300% and 400% FPL saw the biggest increases — the enhanced credits had helped this income band the most. Alabamians under 200% FPL still receive substantial federal APTC, but the cushion is thinner than it was in 2024 and 2025.

| Carrier | 2026 Rate Change | Market Status |

|---|---|---|

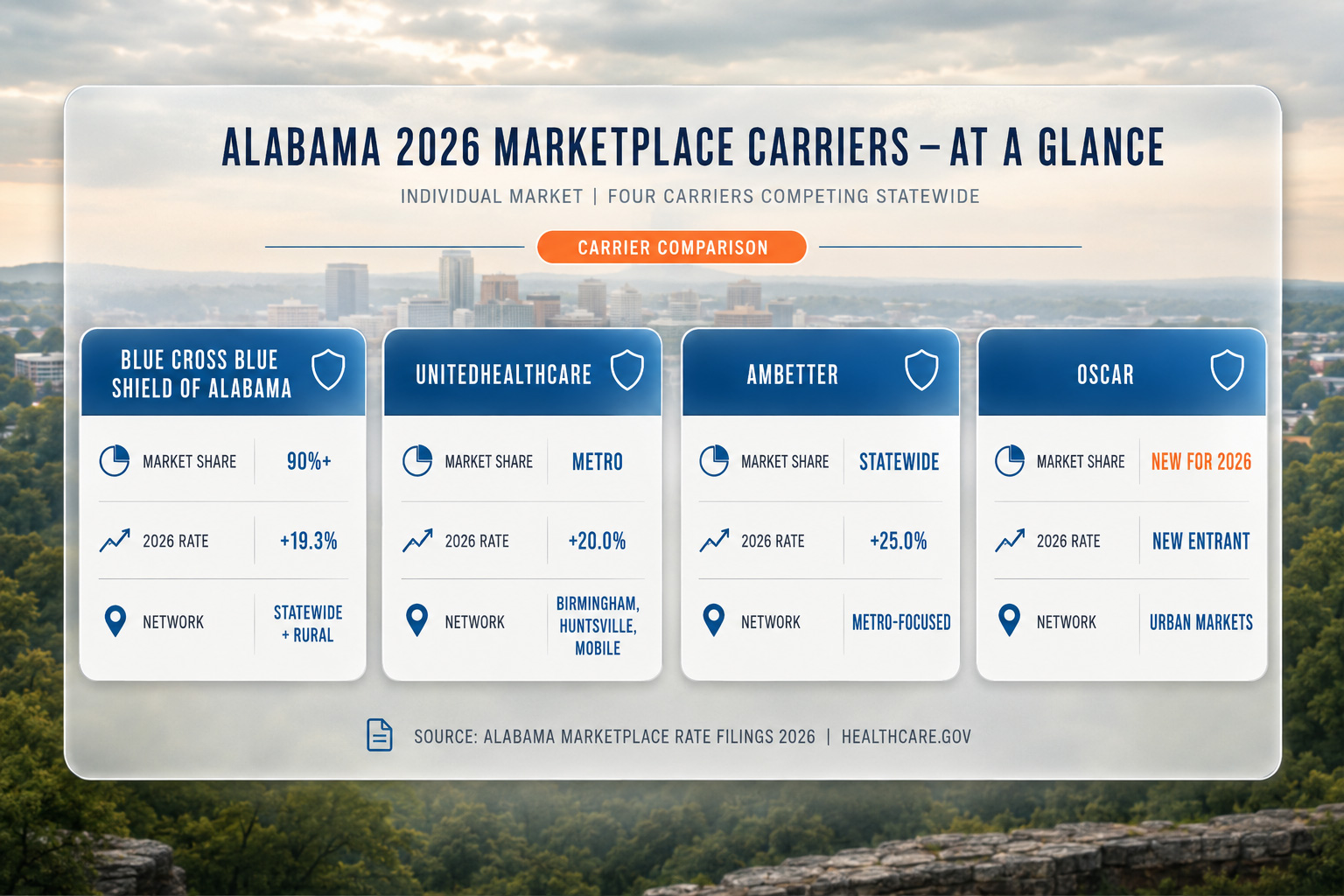

| Blue Cross Blue Shield of Alabama | +19.3% | 90%+ market share — dominant carrier |

| UnitedHealthcare | +20.0% | Metro markets — Birmingham, Huntsville, Mobile |

| Ambetter (Centene) | +25.0% | Statewide — lower premiums, narrower network |

| Oscar Insurance | New to AL | Entered Alabama market for 2026 |

Source: Alabama marketplace 2026 rate filings, Alabama Department of Insurance.

2027 enrollment deadline change: Starting with the 2027 plan year, open enrollment in Alabama ends December 15 — not January 15. The extended January 15 window was a pandemic-era policy that is expiring. Alabamians who miss the December 15, 2026 deadline for 2027 coverage will need a qualifying life event to enroll mid-year.

The Four Carriers on Alabama’s 2026 Marketplace

Four carriers compete on Alabama’s 2026 marketplace: Blue Cross Blue Shield of Alabama, UnitedHealthcare, Ambetter, and Oscar. Blue Cross dominates with over 90% market share and the largest statewide network — critical in rural counties where it is often the only carrier with local in-network providers. The other three carriers are competitive in specific metro markets with more limited rural reach. For network type differences — EPO, HMO, and PPO — see the PPO vs HMO vs EPO guide.

Blue Cross Blue Shield of Alabama

- 90%+ individual market share

- 90-year operating history in Alabama

- Deepest rural county network statewide

- Full integration with UAB Health System

- 2026 rate increase: +19.3%

- Best for: most Alabamians, especially rural and UAB patients

UnitedHealthcare

- Competitive in Birmingham, Huntsville, Mobile metros

- Strong national PPO network for frequent travelers

- 2026 rate increase: +20.0%

- Best for: metro residents who travel frequently

Ambetter (Centene)

- Available statewide on the marketplace

- Typically lower premiums than Blue Cross

- Narrower provider network than Blue Cross

- 2026 rate increase: +25.0%

- Best for: budget-focused enrollees in metro areas

Oscar Insurance

- New to Alabama for 2026

- Tech-forward member tools and virtual care

- Network still being established in Alabama

- Best for: younger, tech-comfortable enrollees in urban markets

What Coverage Costs in Alabama for 2026

Before subsidies, a 40-year-old in Alabama pays $352 to $538 per month for a Silver plan depending on carrier. After federal premium tax credits, the average subsidized Alabama enrollee pays approximately $121 per month for 2026 coverage — up sharply from $44 per month in 2025. Per CMS open enrollment data, 92% of Alabama marketplace enrollees qualified for subsidies in 2025. Premium costs vary by age, plan tier, and carrier.

| Age | Bronze (before subsidies) | Silver (before subsidies) | Gold (before subsidies) |

|---|---|---|---|

| Age 21 | $235 – $320/mo | $280 – $380/mo | $360 – $470/mo |

| Age 30 | $295 – $400/mo | $350 – $480/mo | $450 – $590/mo |

| Age 40 | $340 – $470/mo | $410 – $568/mo | $520 – $690/mo |

| Age 50 | $480 – $650/mo | $580 – $780/mo | $740 – $960/mo |

| Age 60 | $700 – $950/mo | $850 – $1,150/mo | $1,080 – $1,420/mo |

Source: Alabama marketplace 2026 rate filings; age-40 Silver benchmark before subsidies.

These are sticker prices before subsidies. Federal premium tax credits are available to Alabama residents with household income between 100% and 400% FPL — approximately $15,060 to $62,400 for a single adult. There are no state-funded subsidies in Alabama beyond the federal tax credit. For a detailed breakdown of subsidy amounts and real-world cost examples, see the affordable coverage guide.

Scenario: Birmingham family of three, household income $55,000

A family of three in Birmingham — two adults in their late 30s and one child — earns $55,000 annually, placing them at approximately 225% of the 2026 Federal Poverty Level. On the marketplace, they qualify for federal APTC. A Blue Cross Silver family plan sticker price runs approximately $1,650 per month. After premium tax credits, they pay approximately $480 per month — about 10.5% of their household income, the ACA benchmark. They also qualify for cost-sharing reductions on the Silver plan, lowering their deductible and out-of-pocket maximum compared to the standard Silver tier.

Alabama’s Medicaid Coverage Gap

Roughly 90,000 Alabamians fall into a coverage gap because Alabama has not expanded Medicaid under the ACA. These residents earn below $15,060 as a single adult — too little to qualify for marketplace subsidies — but do not meet Alabama’s traditional Medicaid income limits. Alabama is one of 10 states that has not expanded Medicaid as of 2026, leaving this gap unaddressed at the state level.

If you fall into the coverage gap, marketplace plans at full sticker price ($400 to $600 per month for a single adult) are not realistic. The Alabama Medicaid Agency administers traditional Medicaid for children, pregnant women, the elderly, and people with disabilities — but not for most low-income working adults without children. Options for gap residents include short-term health insurance, health sharing ministries, and Federally Qualified Health Centers (FQHCs) that provide care on a sliding-scale fee basis regardless of insurance status.

Short-term plans are not ACA-compliant: Alabama permits short-term plans of up to 364 days with renewals of up to 36 months — more permissive than most states. These plans do not cover pre-existing conditions, do not include essential health benefits, and can deny claims after enrollment if a condition was present before the policy started. They provide limited protection but are better than being uninsured for otherwise healthy gap residents.

How Alabamians Access Health Coverage

Alabama residents access health coverage through six main pathways: the federal marketplace at HealthCare.gov, employer-sponsored plans, Medicare, Medicaid, short-term alternatives, and military or government programs. The right path depends on age, income, employment status, and whether your employer offers coverage. The marketplace is the relevant path for most self-employed Alabamians and those between jobs.

Federal Marketplace (HealthCare.gov)

For self-employed, between jobs, or without employer coverage. Four carriers compete on Alabama’s marketplace. Subsidies available for income $15,060 to $62,400 (single). Alabama does not run a state-based exchange. Self-employed Alabamians can also explore self-employed PPO options. See the Alabama marketplace guide for enrollment details.

Employer-Sponsored Coverage

Employers with 50+ full-time employees must offer coverage under the ACA employer mandate. Employers typically pay 70-80% of premiums. If your employer offers affordable coverage that meets minimum value, you cannot receive marketplace subsidies — even if you’d prefer a marketplace plan.

Medicaid

Traditional Alabama Medicaid covers children, pregnant women, elderly residents, and people with qualifying disabilities. Alabama has not expanded Medicaid to cover low-income working adults without children. The Alabama Medicaid Agency administers the program. See medicaid.alabama.gov for eligibility details.

Medicare

Available at age 65 or with qualifying disability. Medicare Part A covers hospitalization; Part B covers outpatient care; Part D covers prescriptions. Medicare Advantage plans from Alabama carriers offer bundled coverage as an alternative to original Medicare with a supplemental Medigap policy.

Coverage by Region: Networks and Hospitals

Where you live in Alabama determines which carriers have competitive networks and which hospital systems are accessible in-network. Blue Cross covers the entire state, but regional differences in competing carrier availability and hospital network depth affect which plan makes the most sense for your specific location.

Birmingham and Central Alabama

All four carriers operate here with their strongest networks. UAB Health System handles transplants, cancer treatment, and clinical trials unavailable elsewhere. Children’s of Alabama is the top pediatric option. The most competitive carrier pricing in the state — all four carriers compete aggressively here.

Huntsville and Tennessee Valley

Huntsville Hospital handles most specialized needs locally. Major aerospace and defense employers offer strong group plans, but the 2026 Huntsville aerospace layoffs pushed many workers into the individual market. Blue Cross and UnitedHealthcare both have strong Huntsville networks.

Mobile and Gulf Coast

USA Health (University of South Alabama) provides academic medicine on the Gulf Coast. Florida Panhandle hospitals are accessible for some southern Alabama residents. Ambetter has a stronger presence in Mobile than in most other Alabama regions. Blue Cross still leads on network breadth.

Rural Alabama

Blue Cross is often the only carrier with meaningful in-network coverage in rural counties — particularly in the Black Belt region. UnitedHealthcare, Ambetter, and Oscar have limited rural presence. Choosing a non-Blue-Cross plan in rural Alabama often means driving significant distances to find in-network providers.

State Insurance Regulations and the ALDOI

Alabama follows federal ACA rules for marketplace plans and uses HealthCare.gov rather than a state-run exchange. The Alabama Department of Insurance (ALDOI) oversees carrier licensing, rate approvals, and consumer complaints at the state level. Key Alabama-specific rules include short-term plan limits of up to 364 days with renewals allowed up to 36 months — more permissive than most states — and no state-funded subsidies beyond the federal tax credit.

The Alabama Department of Insurance reviews and approves all individual and small group rate filings before carriers can implement increases. The ALDOI does not operate as a full rate regulator — it reviews actuarial filings but cannot reject increases that are actuarially justified. Consumer complaints about claims handling, network adequacy, or billing disputes go to the ALDOI’s consumer services division.

Alabama has not enacted any state-level individual mandate to replace the federal mandate (which was effectively zeroed out starting in 2019). There is no penalty for being uninsured in Alabama beyond the loss of coverage protection. The state also does not fund reinsurance or risk corridor programs, leaving the individual market fully exposed to federal rules. HealthCare.gov remains the sole enrollment portal for individual marketplace plans in Alabama, and CMS publishes annual enrollment data for the Alabama market.

Get a free Alabama health insurance quote

A licensed agent compares all four Alabama carriers, applies your subsidies, and finds the plan that fits your budget and providers — at no cost.

Frequently Asked Questions

What are the best health insurance options in Alabama for 2026?

For most Alabamians buying individual coverage, Blue Cross Blue Shield of Alabama offers the widest provider network and typically the lowest premiums. Three other carriers compete on the federal marketplace: UnitedHealthcare, Ambetter, and Oscar, which entered Alabama for 2026. If your income falls between $15,060 and $62,400 as a single adult, you likely qualify for subsidies that significantly reduce your monthly cost.

How much did Alabama health insurance premiums increase for 2026?

Alabama individual market premiums rose 19% to 25% for 2026. Blue Cross increased rates 19.3%, UnitedHealthcare 20%, and Ambetter 25%. The increases followed the expiration of enhanced federal subsidies at the end of 2025, which caused the average after-subsidy premium to rise from $44 to $121 per month statewide.

Does Alabama have a Medicaid coverage gap?

Yes. Alabama has not expanded Medicaid under the ACA, leaving roughly 90,000 residents in a coverage gap. These residents earn below $15,060 as a single adult — too little for marketplace subsidies but above Alabama’s traditional Medicaid income limits. Options include short-term health insurance, community health centers with sliding-scale fees, and health sharing ministries, though none provide full ACA-compliant coverage.

When is open enrollment for Alabama health insurance?

Open enrollment for 2026 ran November 1, 2025 through January 15, 2026. Alabama uses the federal marketplace at HealthCare.gov — there is no state-based exchange. Outside open enrollment, you can enroll within 60 days of a qualifying life event such as job loss, marriage, or moving. Starting with 2027 coverage, open enrollment will end December 15 instead of January 15.

Why does Blue Cross Blue Shield dominate Alabama’s insurance market?

Blue Cross Blue Shield of Alabama controls over 90% of the individual market because of its 90-year operating history in the state, deep integration with UAB Health System, and the most comprehensive rural county network of any Alabama carrier. For most Alabamians — especially those outside Birmingham, Huntsville, and Mobile — Blue Cross is the only carrier with in-network access to local providers.

What is the income limit for health insurance subsidies in Alabama for 2026?

Federal premium tax credits are available to Alabama residents with household income between 100% and 400% of the Federal Poverty Level — approximately $15,060 to $62,400 for a single adult in 2026. There are no state-funded subsidies in Alabama beyond the federal tax credit. Households below $15,060 may fall into the coverage gap if Alabama’s traditional Medicaid limits are not met.

Related Alabama Health Insurance Resources

Blue Cross, UnitedHealthcare, Ambetter, and Oscar compared — premiums, networks, and fit

Individual Health Insurance AlabamaSelf-employed and individual coverage options through HealthCare.gov for 2026

Affordable Health Insurance AlabamaHow subsidies cut premiums for the 92% of Alabama enrollees who qualify

Alabama Health Insurance MarketplaceEnrollment, deadlines, and subsidy eligibility on the HealthCare.gov marketplace

Alabama Small Business Health InsuranceGroup plans, the SHOP tax credit, and ICHRA for Alabama employers

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required

Ready to find your Alabama health insurance plan?

Compare all four Alabama marketplace carriers with a licensed agent. Subsidies applied, no cost to you.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Alabama residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.