Individual Health Insurance Texas 2026: Personal Plans

Individual health insurance Texas plans for 2026 are purchased directly by a person outside employer group coverage — available through HealthCare.gov marketplace (ACA-compliant, subsidized for qualifying households) or off-exchange from carriers including BCBSTX, Cigna, and UnitedHealthcare. The critical Texas distinction: HealthCare.gov offers only HMO and EPO individual plans — no PPO. Texans who need individual PPO coverage with out-of-network reimbursement and no-referral specialist access must enroll off-exchange.

What brings you here today?

Who Needs Individual Health Insurance in Texas

Individual health insurance Texas coverage is needed by any Texan without employer group benefits — self-employed 1099 contractors, freelancers, sole proprietors, people between jobs, early retirees ages 55–64, part-time and gig workers, adults who aged off a parent’s plan at 26, and higher-income households that want PPO coverage not available on HealthCare.gov. Texas has roughly 3.5 million individual insurance buyers outside employer plans.

The individual health insurance Texas market encompasses everyone who doesn’t access coverage through an employer. Texas has a large self-employed and gig economy workforce — 1099 contractors, rideshare drivers, tradespeople, consultants, and small business owners who don’t participate in group plans. It also includes the growing segment of Texans who have left employer coverage voluntarily — early retirees, people who have reduced work hours, and individuals who prefer the flexibility of individually owned coverage over employer-sponsored plans they don’t control.

A key advantage of individual coverage that many Texans overlook: the plan belongs to you, not your employer. When you leave a job, your individual health insurance Texas plan continues — you don’t lose it, face COBRA decisions, or scramble for a Special Enrollment Period. Off-exchange individual PPO plans in particular are fully portable across job changes, self-employment periods, and life transitions. According to Kaiser Family Foundation data, Texas has the largest share of uninsured residents of any U.S. state — approximately 5 million — many of whom are individual market candidates who lack access to employer coverage. This portability is one of the structural reasons higher-income Texans prefer off-exchange individual PPO over employer group coverage when both are available.

Individual Health Insurance Texas: Subsidy Eligibility

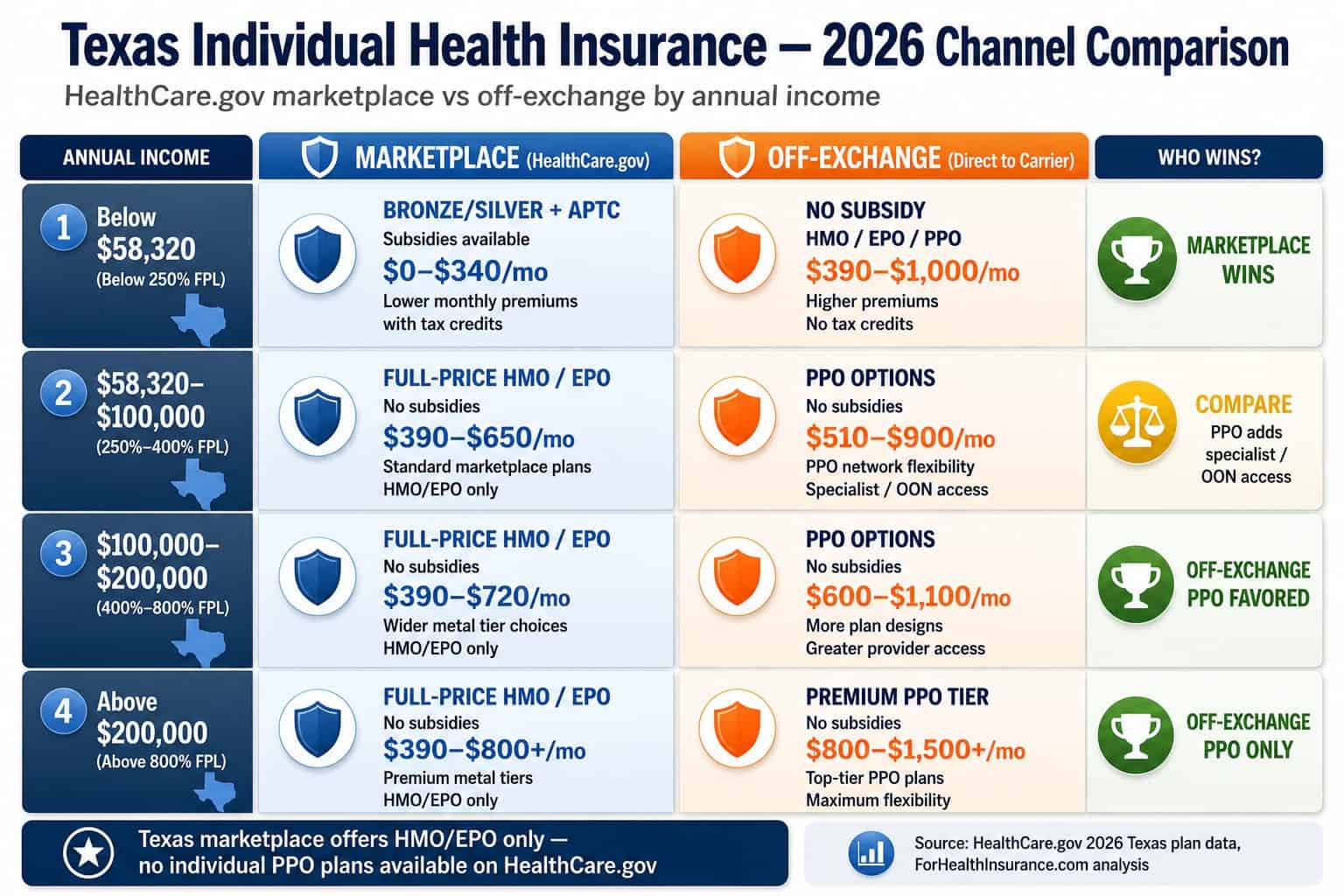

Individual health insurance Texas buyers below 400% of federal poverty level ($60,240 for a single adult in 2026) qualify for Advanced Premium Tax Credit subsidies on HealthCare.gov marketplace plans. The credit reduces monthly premium directly and applies to any metal tier selected. CSR further lowers deductibles for individual buyers below 250% FPL on Silver plans. Above the subsidy ceiling, full-price marketplace and off-exchange premiums are comparable.

| Annual Income (single adult, 2026) | Recommended Channel | Plan Type Available | Typical Net Monthly Premium |

|---|---|---|---|

| Below $15,060 (below 100% FPL) | Coverage gap — no APTC | Catastrophic (hardship exemption) | $210–$280/mo (no subsidy) |

| $15,060–$37,650 (100%–250% FPL) | HealthCare.gov marketplace | Silver + CSR (best value) | $0–$170/mo after APTC+CSR |

| $37,650–$60,240 (250%–400% FPL) | HealthCare.gov marketplace | Silver or Bronze + APTC | $170–$340/mo after APTC |

| $60,240–$120,000 (above 400% FPL) | Off-exchange (HMO/EPO or PPO) | ACA HMO/EPO or PPO | $390–$780/mo full price |

| Above $120,000 | Off-exchange PPO preferred | PPO with OON + national reciprocity | $600–$1,100/mo |

For individual health insurance Texas buyers on HealthCare.gov, the subsidy calculation uses Modified Adjusted Gross Income — not gross income or total household income without adjustments. For a self-employed Texan, MAGI is primarily Schedule C net income plus other taxable income. For an employed Texan who has left a job, MAGI includes severance, unemployment benefits if received, investment income, and any part-year W-2 earnings. Roth IRA withdrawals and home equity proceeds do not count toward MAGI. The MAGI figure entered on HealthCare.gov determines APTC amount — and must be updated if actual income tracks significantly differently from the projection mid-year.

Texans above the 400% FPL APTC ceiling get no subsidy regardless of which channel they use. At that income level, coverage on-exchange (HealthCare.gov) and off-exchange (direct carrier) costs similar monthly premiums for ACA-compliant plans — but off-exchange adds the PPO option unavailable on the Texas marketplace. For higher-income individual buyers, the off-exchange channel is almost always the more relevant comparison. See private health insurance Texas for the detailed on-exchange vs off-exchange cost modeling for individual buyers by income tier.

Individual PPO Plans in Texas: Off-Exchange Only

Individual PPO health insurance in Texas is available exclusively off-exchange — no individual PPO plans are sold on HealthCare.gov in Texas. Off-exchange individual PPO plans from BCBSTX, Cigna, UnitedHealthcare, Aetna, and Humana provide out-of-network reimbursement, no-referral specialist access, and national network reciprocity. Premiums run $510–$1,000+ monthly for a 40-year-old depending on carrier and tier. No APTC subsidies apply.

The individual PPO product is the premium segment of Texas individual health insurance — priced higher than marketplace HMO and EPO plans, but delivering coverage capabilities those plans lack. Out-of-network reimbursement means a Tyler East Texas contractor who sees a specialist at UT Southwestern in Dallas and a primary care provider at a local East Texas clinic can use both in-network at their PPO plan’s contracted rates without needing to choose one network. The same contractor traveling to a project in Colorado uses their BlueCard (BCBSTX) or Open Access Plus (Cigna) national network at in-network rates — not the out-of-network penalty a marketplace HMO plan would impose.

For individual health insurance Texas buyers considering PPO coverage, the Texas PPO Plans guide covers the five-carrier landscape in depth — BCBSTX, Cigna, UnitedHealthcare, Aetna, and Humana — with 2026 premium ranges by rating area, hospital system network contracting, and the national PPO hub at PPO health insurance plans for cross-state context. Individual PPO enrollment is year-round with no open enrollment restriction — a meaningful flexibility advantage over HealthCare.gov marketplace enrollment windows.

Example: Austin Software Engineer, Age 35 — On-Exchange vs Off-Exchange

A 35-year-old software engineer in Travis County goes independent after leaving a tech employer. His projected Schedule C net income is $68,000 — above the $60,240 single-adult APTC ceiling, so no HealthCare.gov subsidy applies. He compares two paths: an Ambetter Silver EPO on HealthCare.gov at full price runs approximately $545/month. A BCBSTX Blue Advantage PPO off-exchange runs approximately $820/month — $275 more but with out-of-network coverage, no referrals, and BlueCard national reciprocity. He evaluates a middle option: a BCBSTX Silver EPO off-exchange at $590/month — nearly identical coverage to the marketplace HMO but available year-round without an open enrollment window. He chooses the off-exchange Silver EPO for the $45/month premium difference over marketplace and year-round enrollment flexibility, accepting the lack of PPO out-of-network coverage as an acceptable trade-off for his current health utilization.

Get an Individual Texas Health Insurance Quote

A licensed Texas broker compares individual health insurance Texas options across HealthCare.gov marketplace plans and off-exchange PPO products from BCBSTX, Cigna, and UnitedHealthcare — with APTC subsidy calculation and provider network verification. Free, no obligation.

Texas Individual Health Insurance Carriers for 2026

Individual health insurance Texas buyers choose from two carrier groups depending on channel. On HealthCare.gov, BCBSTX leads on statewide network depth, Ambetter on lowest premium, and Oscar on digital member experience. Off-exchange, BCBSTX and Cigna lead the individual PPO market for above-subsidy buyers, with UnitedHealthcare Choice Plus PPO carrying the strongest national network for Texans who travel.

Blue Cross Blue Shield of Texas (BCBSTX)

On + Off ExchangeThe dominant individual health insurance Texas carrier in both channels. Statewide HealthCare.gov presence across all 26 rating areas with Bronze, Silver, and Gold HMO/EPO plans. Off-exchange individual PPO with BlueCard national reciprocity — Memorial Hermann, Houston Methodist, Baylor Scott & White, Texas Health Resources, HCA Healthcare all in-network. Strongest fit for individual buyers who value network breadth and statewide access.

- On-exchange and off-exchange products

- All 26 Texas rating areas

- Broadest individual network

- BlueCard PPO national reciprocity

Ambetter (Centene)

On-exchange / Lowest costLowest-premium individual plans on HealthCare.gov across most Texas rating areas — the go-to for subsidy-eligible individual buyers prioritizing monthly cost. Bronze and Silver CSR plans consistently $30–$70 below BCBSTX for equivalent tiers. Network is narrower, strongest in Houston, DFW, Austin, San Antonio metros. On-exchange only — no individual off-exchange PPO product.

- Lowest on-exchange individual premium

- CSR Silver specialist

- Major metro network

- On-exchange only

Cigna

Off-exchange PPOOpen Access Plus individual PPO — the strongest off-exchange PPO choice for above-subsidy Texas individual buyers in Houston, DFW, Austin, and San Antonio. National reciprocity for individual buyers who work across state lines. Off-exchange only in Texas — no HealthCare.gov marketplace product. Premium runs $550–$950/month for a 40-year-old depending on tier. Best fit: individual buyers above subsidy ceiling who need out-of-network coverage.

- Off-exchange individual PPO only

- Open Access Plus network

- Strong national reciprocity

- Metro-anchored Texas coverage

Oscar Health

Digital / On-exchangeIndividual HMO and EPO plans on HealthCare.gov in Houston, DFW, Austin, and San Antonio with 24/7 telehealth included and digital care team. Mid-range premium between Ambetter and BCBSTX. Strong fit for digitally native individual buyers who prefer app-based member management and virtual care integration. On-exchange only — no off-exchange individual product.

- Major Texas metros only

- 24/7 telehealth included

- Digital-first individual experience

- On-exchange only

UnitedHealthcare

National / Travel-friendlyIndividual on-exchange plans in select Texas rating areas and Choice Plus PPO off-exchange statewide. The broadest national individual network of any Texas carrier — individual buyers who travel for work or split time between states benefit from UHC’s seamless in-network access anywhere in the country. HSA-eligible individual HDHP variants available off-exchange for tax-stacking individual buyers.

- Select rating areas on-exchange

- Choice Plus individual PPO off-exchange

- Broadest national network

- HSA-eligible individual HDHP option

Aetna

Select metrosIndividual on-exchange plans in select Texas rating areas with CVS MinuteClinic integration. Mid-range premium on-exchange. Primarily employer group-focused off-exchange. Strongest for individual buyers in Dallas-Fort Worth and Houston metros who value CVS pharmacy network depth and MinuteClinic access as part of their individual plan’s routine care toolkit.

- Select Texas metro availability

- CVS/MinuteClinic integration

- Mid-range individual premium

- Group-focused off-exchange

Individual Health Insurance Texas: Enrollment and Timing

Individual health insurance Texas enrollment timing depends on channel. HealthCare.gov marketplace enrollment is restricted to the November 1 through January 15 open enrollment window annually, or a qualifying SEP within 60 days of a life event. Off-exchange individual plans — including individual PPO from BCBSTX, Cigna, and UnitedHealthcare — are available year-round with no enrollment window restriction, making off-exchange the faster path when individual coverage is needed immediately.

The year-round availability of off-exchange individual plans in Texas is a significant practical advantage over HealthCare.gov enrollment. A 38-year-old Tyler consultant who signs a new contract in March has no HealthCare.gov open enrollment to access — unless the contract start triggers a Special Enrollment Period (which it won’t unless it involves losing existing job-based coverage). An off-exchange individual PPO application submitted in March gets an April 1 effective date in most cases. For individual buyers who need coverage immediately outside of open enrollment and don’t have a qualifying SEP, off-exchange is typically the only route to ACA-compliant individual coverage.

For individual buyers who do have a qualifying SEP or are in open enrollment, the Texas health insurance marketplace guide covers the full HealthCare.gov enrollment process, subsidy eligibility step-by-step, and plan selection strategy. The Texas Department of Insurance licenses all carriers serving this market and maintains a public broker and carrier lookup for verifying any agent or company before enrolling.

Frequently Asked Questions

Common questions about individual health insurance Texas cover what individual coverage means (not employer group), whether individual PPO plans exist in Texas (yes, off-exchange only), 2026 individual premium ranges by income and age, who specifically needs individual coverage, and the difference between individual and family plans in the Texas marketplace context.

What is individual health insurance in Texas?

Individual health insurance Texas refers to coverage purchased by a person directly — not through an employer’s group plan. It covers a single adult or a single adult plus dependents under a plan the individual owns and controls. Individual health insurance Texas is available through two channels: HealthCare.gov for ACA-compliant plans with Advanced Premium Tax Credit subsidy eligibility, and off-exchange directly from carriers such as BCBSTX, Cigna, UnitedHealthcare, and Humana. Off-exchange individual plans include PPO options unavailable on the Texas marketplace, making off-exchange the required path for Texans who need out-of-network coverage or no-referral specialist access.

Can I get a PPO as individual health insurance in Texas?

Yes — but only off-exchange, not through HealthCare.gov. The Texas federal marketplace offers only HMO and EPO individual plans; no individual PPO plans are sold on HealthCare.gov in Texas. Texans who want a PPO for individual coverage must enroll directly with a carrier or through a licensed Texas broker off-exchange. BCBSTX, Cigna, UnitedHealthcare, and Humana offer individual PPO plans off-exchange in Texas. Note: Aetna exited the individual market entirely at end of 2025 and is no longer available for individual enrollment. Off-exchange PPO enrollment forfeits Advanced Premium Tax Credit subsidy eligibility — making PPO the right individual plan choice primarily for Texans above the 400% FPL subsidy ceiling ($60,240 for a single adult in 2026) or those with specific specialist or out-of-network care needs that justify the higher premium.

How much does individual health insurance cost in Texas for 2026?

Individual health insurance Texas costs for 2026 vary by age, plan tier, rating area, and subsidy eligibility. At full price, a 40-year-old non-smoker pays $390–$520 monthly for Bronze and $460–$580 for Silver on HealthCare.gov before subsidies. After APTC, a 40-year-old earning $40,000 typically pays $80–$160 monthly for Silver. Off-exchange individual PPO plans for the same age run $510–$1,000+ monthly depending on tier and carrier. Texas operates 26 geographic rating areas — Houston, Dallas-Fort Worth, and Austin generally carry lower individual premiums than rural West Texas or the Rio Grande Valley.

Who needs individual health insurance in Texas?

Individual health insurance Texas coverage is needed by any Texan without access to employer-sponsored group coverage — self-employed people including 1099 contractors, freelancers, and sole proprietors; people between jobs who have declined or exhausted COBRA; early retirees ages 55–64 bridging to Medicare; part-time or gig economy workers without employer benefits; adults who have aged off a parent’s plan at 26; and Texans above income limits for Medicaid who don’t have employer coverage. Individual coverage is also the right path for Texans above employer plan subsidy ceilings who want PPO network access not available on HealthCare.gov in Texas.

What is the difference between individual and family health insurance in Texas?

Individual health insurance Texas covers a single enrollee — one adult — while family plans extend coverage to a spouse and dependent children on the same policy. For ACA marketplace plans, the premium increases for each additional covered person up to three children, after which additional children are typically added at no extra premium cost. Texas families with children below 200% of federal poverty level ($62,400 for a family of four in 2026) often save more by splitting coverage — enrolling children in Texas CHIP at near-zero cost and parents in individual marketplace plans with APTC subsidies — rather than a single family marketplace plan covering everyone.

Compare 2026 Individual Texas Health Insurance

A licensed Texas broker compares individual health insurance Texas options across on-exchange HealthCare.gov plans and off-exchange individual PPO products from BCBSTX, Cigna, and UnitedHealthcare — with APTC subsidy calculation, rating area pricing, and provider network verification. Free, no obligation.

Free Texas individual coverage comparison — marketplace and off-exchange PPO in one call.

Explore Texas Coverage In Depth

Statewide overview — marketplace, Medicaid gap, off-exchange, and all carrier options.

Texas Marketplace EnrollmentHealthCare.gov guide for individual Texas buyers — APTC subsidies, open enrollment, and SEPs.

Texas PPO PlansIndividual off-exchange PPO options — BCBSTX, Cigna, UHC compared with network depth.

Self-Employed Texas Health InsuranceIndividual coverage for 1099 contractors — Schedule 1 deduction, HSA stacking, MAGI strategy.

Cheap Texas Health InsuranceLowest-cost individual plans — subsidized Bronze and Silver for qualifying Texas buyers.

Catastrophic Texas Health InsuranceIndividual under-30 marketplace plans — lowest ACA-compliant premium tier.

Short-Term Texas Health InsuranceNon-ACA individual bridge coverage for Texans between employer plans.

Private Texas Health InsuranceOn-exchange vs off-exchange individual coverage — subsidy trade-off and direct carrier enrollment.

Family Texas Health InsuranceCHIP split-enrollment, maternity coverage, family glitch fix, and household cost strategies.

Texas Retiree Health InsurancePre-Medicare bridge ages 55–64 — TRS-Care, ERS, APTC subsidies, COBRA vs marketplace.

Texas Small Business Health InsuranceGroup plans for 1–50 employees — PPO, HMO, SHOP, and ICHRA options compared.

National PPO Health Insurance PlansNationwide PPO guidance applying across all 50 states — carriers, networks, and rate structures.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Texas residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.