Texas Health Insurance 2026: Plans, Costs & Enrollment

Texas health insurance in 2026 is shaped by three structural facts unique to the state: Texas uses HealthCare.gov rather than a state-based exchange, Texas has not expanded Medicaid (leaving roughly 1.5 million adults in a coverage gap), and HealthCare.gov in Texas offers only HMO and EPO plans — no PPO products. Approximately 3.2 million Texans enrolled in marketplace plans for 2026, the most of any state. Average subsidized premium: $67 per month.

Find your Texas coverage path

Texas Health Insurance at a Glance

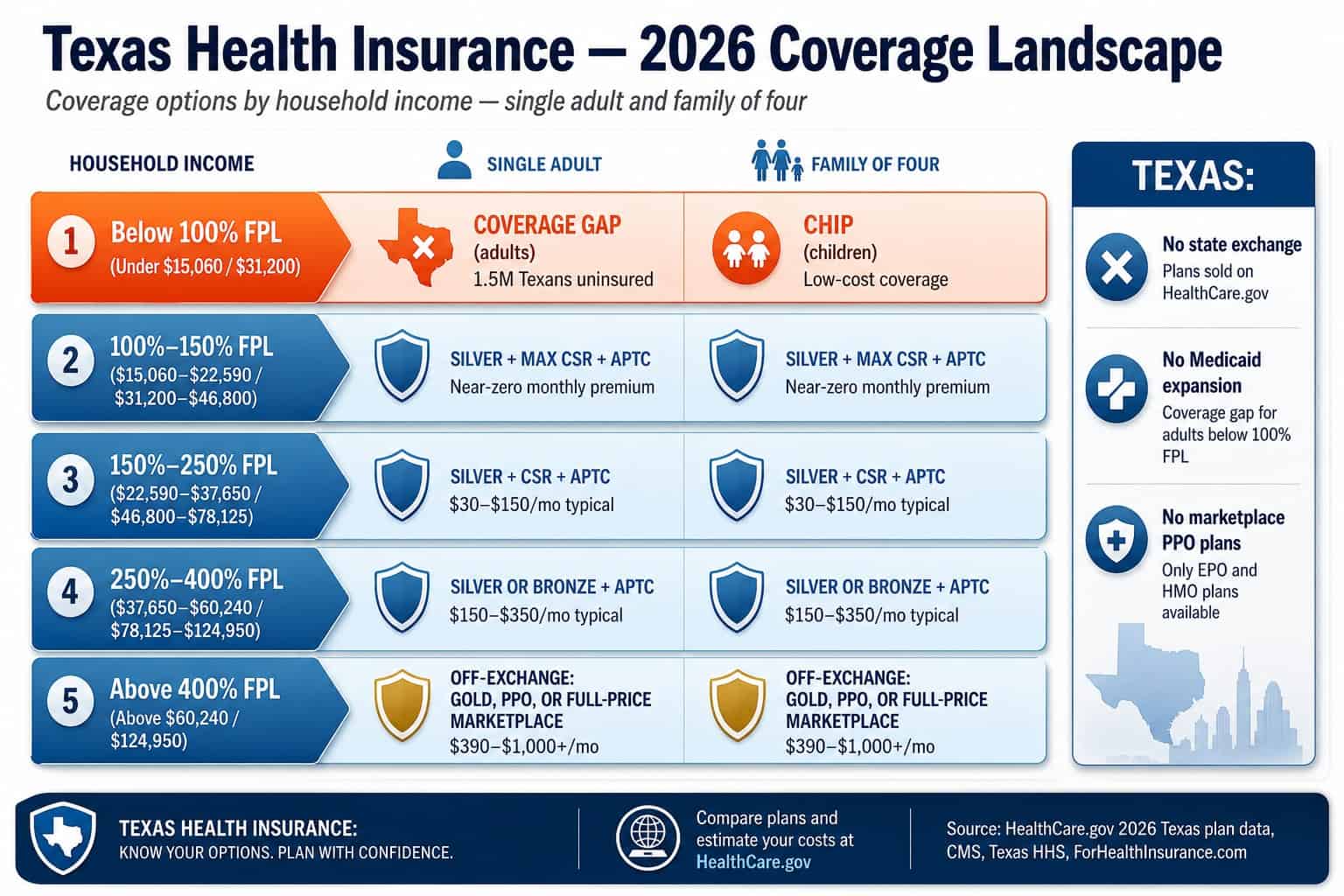

Texas health insurance in 2026 is available through four primary paths: HealthCare.gov marketplace plans (ACA-compliant, subsidized for qualifying households), off-exchange plans directly from carriers (PPO available, no subsidies), Texas state employee and teacher programs (ERS and TRS-Care), and Medicaid for qualifying adults and CHIP for children under 19. Texas had 3.2 million marketplace enrollees for 2026 — the highest of any state — with 92% receiving Advanced Premium Tax Credit subsidies.

Texas is the largest and most complex individual health insurance market in the United States. With 29 million residents, the highest uninsured rate of any state, and no state-based exchange, the Texas coverage market operates entirely through the federal HealthCare.gov portal for on-exchange coverage and through carrier-direct or broker enrollment for off-exchange products. The Texas Department of Insurance regulates all carriers operating in the state — rate filings, network adequacy standards, and consumer complaint resolution — but the exchange infrastructure and subsidy administration are federal.

The scale of Texas marketplace enrollment makes the state’s policy decisions nationally significant. Texas’s choice not to expand Medicaid leaves roughly 1.5 million adults in the coverage gap — the largest coverage gap population of any state, representing approximately 40% of all coverage-gap adults nationwide according to Kaiser Family Foundation analysis. At the same time, expanded APTC subsidies from the Inflation Reduction Act (originally through 2025, extended through 2026 in subsequent legislation) drove Texas marketplace enrollment to record levels — with premium tax credits averaging $667 per month per enrollee for 2026 coverage according to CMS enrollment data.

The Texas Medicaid Coverage Gap

Texas has not expanded Medicaid under the ACA — leaving roughly 1.5 million adults in the coverage gap between traditional Texas Medicaid eligibility (very narrow: parents below 17% of federal poverty level, pregnant women, disabilities) and HealthCare.gov subsidy access (which requires 100% FPL minimum income of $15,060 for a single adult in 2026). Adults in the gap are typically the working poor — too poor for subsidies, ineligible for Medicaid, no employer coverage.

Traditional Texas Medicaid is among the most restrictive in the country. Texas covers parents with household income below roughly 17% of federal poverty level (approximately $4,400 annually for a family of four) — one of the lowest income thresholds for parental Medicaid of any state. Childless adults in Texas are generally not eligible for Medicaid at any income level. Pregnant women qualify for Medicaid through 60 days postpartum up to 198% of federal poverty level. People with qualifying disabilities access Medicaid through SSI and related programs. This means a 35-year-old working Texas adult earning $12,000 annually — below the $15,060 threshold for marketplace subsidies — has no affordable coverage path under current law.

The coverage gap is uniquely a consequence of the Supreme Court’s 2012 NFIB v. Sebelius decision, which made Medicaid expansion optional for states. As of 2026, Texas remains one of ten states that have not expanded. Texas legislators have considered expansion proposals but none have advanced. For Texans in the gap, the practical options include the hardship exemption pathway to ACA catastrophic plans, Texas CHIP for children regardless of adult status, federally qualified health center sliding-scale primary care, and county-level indigent care programs in Harris, Bexar, and Dallas counties.

If your income is below $15,060 (single) — check these options first

Texans below the marketplace subsidy floor should check: (1) Texas CHIP for children under 19 regardless of adult eligibility, apply at YourTexasBenefits.com; (2) Federally Qualified Health Centers across Texas offer sliding-scale primary care at $20–$40 per visit regardless of insurance status; (3) HealthCare.gov hardship exemption for catastrophic plan access — the Medicaid gap is a certified qualifying hardship; (4) Pregnancy Medicaid if applicable — covers prenatal care up to 198% FPL; (5) County hospital district programs in Harris, Bexar, and Dallas counties for limited inpatient and specialist care.

Texas Health Insurance Costs for 2026

Texas health insurance premiums for 2026 vary by age, tier, income, and rating area. Full-price Silver for a 40-year-old runs $460–$580 monthly; after APTC at $40,000 income, the same plan costs $80–$160. A family of four earning $80,000 pays $300–$600 monthly for Silver after subsidies. Texas’s 26 rating areas produce meaningful geographic variation — Houston, Dallas-Fort Worth, and Austin run lower than rural West Texas and the Rio Grande Valley.

| Household Income (2026) | Single Adult Typical Cost | Family of 4 Typical Cost | Best Plan Type |

|---|---|---|---|

| Below $15,060 (below 100% FPL) | Coverage gap — no APTC | Below $31,200 — coverage gap | CHIP for children; hardship exemption for catastrophic |

| $15,060–$22,590 (100%–150% FPL) | $0–$30/mo (max CSR Silver) | $0–$60/mo (family max CSR) | Silver + 94% CSR — best total value |

| $22,590–$37,650 (150%–250% FPL) | $30–$150/mo | $60–$300/mo | Silver + CSR — strong value |

| $37,650–$60,240 (250%–400% FPL) | $150–$350/mo | $300–$600/mo | Silver or Bronze — APTC only |

| Above $60,240 (above 400% FPL) | $390–$1,000+/mo (full price) | $1,400–$2,500+/mo (full price) | Off-exchange Gold or PPO |

Pricing across the state’s 26 rating areas creates a meaningful cost gap between major metro and rural markets. A 40-year-old buying a BCBSTX Silver plan in Houston (rating area 18) or Dallas-Fort Worth (rating area 8) typically pays $460–$510/month at full price; the same plan in rural West Texas rating areas can run $560–$640/month — reflecting thinner provider networks, higher local claims experience, and fewer carriers competing for enrollment. The most affordable Texas metro markets are generally Dallas-Fort Worth, Houston, and Austin; the highest-cost rating areas are in the Rio Grande Valley, West Texas Panhandle, and East Texas border regions.

Plan Types in Texas: HMO, EPO, PPO, and Catastrophic

Texas health insurance plan types split along the on-exchange vs off-exchange divide. HealthCare.gov in Texas offers HMO and EPO plans only — no individual PPO products are sold on the federal marketplace in Texas. Off-exchange direct carrier enrollment unlocks PPO plans from BCBSTX, Cigna, UnitedHealthcare, Aetna, and Humana. Catastrophic plans are available on HealthCare.gov for Texans under 30 or with a qualifying hardship exemption.

The absence of PPO plans on HealthCare.gov in Texas is the single structural difference between Texas and states with state-based exchanges that certify PPO products. HMO plans require a primary care physician as a gatekeeper for specialist referrals and restrict coverage to network providers — no out-of-network reimbursement except in emergencies. EPO plans skip the PCP gatekeeper requirement (direct specialist access) but still restrict coverage to network providers with no out-of-network benefits. PPO plans — available only off-exchange in Texas — allow both direct specialist access and out-of-network coverage at reduced reimbursement rates, plus national reciprocity through BlueCard (BCBSTX), Open Access Plus (Cigna), and Choice Plus (UHC) networks.

For Texans who specifically need PPO access — frequent travelers, patients with multi-system specialist care, households with providers at multiple Texas hospital systems — the coverage choice is entirely off-exchange. See the Texas PPO Plans guide for detailed carrier comparison, 2026 premium ranges, and the 26-rating-area pricing landscape. For nationwide context on PPO plan structures across all 50 states, the PPO health insurance plans hub covers the full national picture. For subsidy-eligible Texans content with HMO or EPO network access, HealthCare.gov delivers substantially lower net premium after APTC than any off-exchange equivalent.

Texas Health Insurance Carriers for 2026

Individual and family health plans in Texas for 2026 are available from seven primary carriers across on-exchange and off-exchange channels. On HealthCare.gov, the dominant carriers are Blue Cross Blue Shield of Texas (BCBSTX), Ambetter (Centene), Oscar Health, Aetna, and UnitedHealthcare, with availability varying by rating area. Off-exchange, BCBSTX, Cigna, UnitedHealthcare, Aetna, and Humana offer ACA-compliant and non-compliant individual products through direct carrier or broker enrollment.

Blue Cross Blue Shield of Texas (BCBSTX)

HCSC subsidiary and the largest individual health insurance carrier in Texas by enrollment. BCBSTX is available across all 26 rating areas on HealthCare.gov and off-exchange, with the deepest provider network at Memorial Hermann, Houston Methodist, Baylor Scott & White, Texas Health Resources, and HCA Healthcare. Broadest pediatric specialist access. BlueCard national reciprocity off-exchange.

Ambetter (Centene)

Centene’s Texas marketplace brand and consistently the lowest-premium Bronze and Silver carrier on HealthCare.gov across most Texas rating areas. CSR Silver specialist. Narrower network than BCBSTX, concentrated in Houston, DFW, Austin, and San Antonio. On-exchange only — no off-exchange product line.

Oscar Health

On-exchange HMO and EPO plans in Houston, DFW, Austin, and San Antonio with 24/7 telehealth and a digital care team. Mid-range premium between Ambetter and BCBSTX. Strong fit for tech-comfortable Texas enrollees who prefer app-based member management. Major metro network.

Cigna

Open Access Plus PPO — the leading off-exchange PPO carrier for above-subsidy Texas households in Houston, DFW, Austin, and San Antonio. Off-exchange only in Texas. Strong national reciprocity for Texans who travel or work cross-state.

UnitedHealthcare

On-exchange in select Texas rating areas; Choice Plus PPO off-exchange statewide. Broadest national network of any Texas carrier — the top choice for multi-state travelers and snowbirds. CVS MinuteClinic integration for Aetna. Selective metro availability on-exchange.

Aetna

On-exchange in select Texas metros with CVS Health integration — MinuteClinic access and CVS pharmacy depth. Mid-range premium on-exchange. Primarily employer-group focus off-exchange. Strongest in Dallas-Fort Worth and Houston on-exchange markets.

Get a Texas Health Insurance Quote

A licensed Texas broker compares all 2026 HealthCare.gov plans by rating area with full APTC and CSR subsidy calculation, checks CHIP eligibility for children, models off-exchange PPO options for above-subsidy households, and verifies provider network access at Memorial Hermann, Houston Methodist, Baylor Scott & White, and Texas Health Resources. Free, no obligation.

How to Enroll in Texas Health Insurance

Enrollment in Texas health plans runs through two channels: HealthCare.gov for on-exchange ACA-compliant plans with subsidy eligibility, open November 1 through January 15 annually, and direct carrier or broker enrollment for off-exchange products year-round. Texas does not operate a state-based exchange — all marketplace enrollment is federal. The Texas Department of Insurance licenses all carriers and navigators operating in the state.

On-exchange enrollment at HealthCare.gov is the primary path for most Texas households. Create an account, enter household information and projected income, and receive real-time APTC calculations before plan selection. Open enrollment runs November 1 through January 15 for the following plan year — plans selected by December 15 take effect January 1; plans selected December 16 through January 15 take effect February 1. Outside open enrollment, Texans access HealthCare.gov through a qualifying Special Enrollment Period within 60 days of a triggering life event: job loss and loss of job-based coverage, marriage or divorce, birth or adoption, moving to a new Texas rating area, or aging off a parent’s plan at 26.

Off-exchange enrollment goes directly to carriers — BCBSTX, Cigna, UnitedHealthcare, Aetna — through their websites or through a licensed Texas broker. Most off-exchange carriers issue coverage with a first-of-the-month effective date when applications are received by the 15th of the prior month, meaning enrollment is available every month of the year. The Texas Department of Insurance (TDI) maintains a public license lookup for Texas-licensed health insurance carriers, brokers, and navigators — useful for verifying any agent or carrier before enrolling.

Texas-Specific Coverage Programs

Texas operates several coverage programs beyond HealthCare.gov marketplace plans. Texas CHIP covers children under 19 in families below 200% of federal poverty level at near-zero cost. ERS provides retiree and active employee coverage for Texas state agency workers. TRS-Care serves retired Texas public school teachers. Medicaid covers qualifying adults (very narrow eligibility), pregnant women to 198% FPL, children, and people with disabilities.

Texas CHIP (Children’s Health Insurance Program) is the most accessible Texas-specific program — available to children under 19 in families earning below $62,400 (200% FPL for a family of four in 2026) with near-zero enrollment fees and comprehensive coverage including dental and vision. Apply at YourTexasBenefits.com year-round. The Teacher Retirement System of Texas TRS-Care program covers approximately 260,000 retired public school educators and their dependents — TRS-Care Standard for pre-Medicare retirees, TRS-Care Medicare Advantage for Medicare-eligible retirees. The Employees Retirement System of Texas (ERS) provides HealthSelect of Texas and other health plan options for active and retired state agency employees at group rates substantially below individual marketplace premiums.

For detailed guidance on each program, see the dedicated cluster pages: Texas Family Health Insurance covers CHIP split-enrollment strategy; Texas Retiree Health Insurance covers TRS-Care and ERS in depth; Cheap Texas Health Insurance covers the Medicaid gap workarounds and subsidy ladder by income tier.

Texas Health Insurance by Situation

Coverage needs vary significantly by life situation in Texas. Self-employed Texans navigate HealthCare.gov marketplace plans with MAGI income projection and the Schedule 1 tax deduction stack. Families often use CHIP split-enrollment for children. Retirees ages 55–64 need pre-Medicare bridge coverage before Medicare eligibility. Young adults under 30 can access catastrophic plans at lower premium. The right path depends on income, household composition, and provider preferences.

Self-Employed Texans

Self-employed Texans deduct 100% of qualifying premiums on Schedule 1 of Form 1040. Most fall within APTC subsidy bands on HealthCare.gov — making subsidized Silver or Bronze the primary coverage vehicle. Above-subsidy income households access off-exchange PPO or HSA-eligible HDHP plans. See the self-employed Texas health insurance guide for MAGI projection, HSA stacking, and carrier comparison.

Texas Families

Texas families below 200% FPL often achieve lowest total cost through CHIP split-enrollment — children on CHIP, adults on subsidized HealthCare.gov plans. ACA family glitch fix (effective 2023) opened marketplace subsidy eligibility for dependents with expensive employer family coverage. See family health insurance Texas for household strategy.

Pre-Medicare Retirees

Early Texas retirees navigate ACA age-band pricing (64-year-olds pay 3x the 21-year-old rate) with APTC subsidies that often offset much of the increase for moderate-income retirees. TRS-Care and ERS programs serve Texas public employees. See retiree health insurance Texas for the COBRA vs marketplace decision and MAGI management strategies.

Young Adult Texans

Young Texas adults have access to ACA catastrophic plans with the lowest marketplace premium tier — $210–$280/month for a 25-year-old versus $280–$370 for Bronze. Catastrophic is not subsidized, so subsidy-eligible young Texans typically do better on Bronze or Silver. See catastrophic health insurance Texas for the eligibility rules, $10,600 deductible, and carrier comparison.

Budget-Constrained Texans

Texans seeking the lowest possible monthly premium start with APTC-subsidized Bronze or Silver on HealthCare.gov. Below 250% FPL, Silver with CSR often delivers better total value than Bronze due to dramatically lower deductibles. See cheap Texas health insurance for the full affordability ladder and CHIP eligibility guidance.

Coverage Gap Texans

Texans between employer plans can use COBRA continuation (18 months, full premium), ACA marketplace SEP enrollment within 60 days of job loss, or short-term limited-duration plans for bridges up to 36 months. See short-term Texas health insurance for the non-ACA alternative analysis and carrier comparison.

Frequently Asked Questions

Common questions about coverage in Texas cover whether the state has its own marketplace (it does not — HealthCare.gov is the only on-exchange portal), why Texas has the highest uninsured rate in the country (Medicaid non-expansion plus low-wage workforce), 2026 premium costs by age and income, whether PPO plans are available on HealthCare.gov in Texas (they are not), and open enrollment dates for 2026 Texas marketplace coverage.

Does Texas have a state health insurance marketplace?

No. Texas does not operate a state-based health insurance exchange. Texas residents use the federal HealthCare.gov marketplace to enroll in ACA-compliant individual and family health insurance plans. Texas is one of the largest states by population to rely entirely on the federal exchange — which means all marketplace enrollment, subsidy calculation, and plan shopping happens at HealthCare.gov. Texas enrolled approximately 3.2 million residents in marketplace plans for 2026 coverage, the highest total of any state. The Texas Department of Insurance (TDI) regulates carrier rates, network adequacy, and consumer complaints, but the exchange itself is operated by the federal government.

Why does Texas have the highest uninsured rate in the United States?

Texas has the highest uninsured rate of any U.S. state — approximately 17–18% of residents, roughly 5 million people — for two primary structural reasons. First, Texas has not expanded Medicaid under the Affordable Care Act, leaving approximately 1.5 million low-income adults in the coverage gap: earning too much for traditional Texas Medicaid but too little for HealthCare.gov APTC subsidies, which require income at or above 100% of federal poverty level. Second, Texas has a large low-wage service sector and agricultural workforce where employer-sponsored insurance is less common than in states with more concentrated professional employment. The combination of Medicaid non-expansion and high rates of uninsured low-wage workers creates the largest uninsured population by both number and percentage of any U.S. state.

How much does health insurance cost in Texas for 2026?

Texas health insurance costs in 2026 vary significantly by age, plan tier, rating area, and subsidy eligibility. At full price, a 40-year-old non-smoker can expect to pay $390–$520 monthly for Bronze, $460–$580 for Silver, and $590–$720 for Gold on HealthCare.gov before subsidies. After Advanced Premium Tax Credit, the same 40-year-old earning $40,000 typically pays $80–$160 monthly for Silver coverage. A family of four earning $80,000 typically pays $300–$600 monthly for marketplace Silver after subsidies. Texas operates 26 geographic rating areas — Houston, Dallas-Fort Worth, and Austin generally see lower premiums than rural West Texas and the Rio Grande Valley. The average subsidy amount for Texas marketplace enrollees is $667 per month according to CMS 2026 enrollment data.

Can I get a PPO plan on the Texas health insurance marketplace?

No. HealthCare.gov in Texas offers only HMO and EPO plan types for individual coverage — no PPO plans are available on the federal marketplace in Texas. Texans who want a true PPO plan with out-of-network coverage and no-referral specialist access must enroll off-exchange, purchasing directly from carriers such as BCBSTX, Cigna, UnitedHealthcare, Aetna, or Humana. Off-exchange PPO enrollment forfeits Advanced Premium Tax Credit subsidy eligibility. For Texans who need PPO network access and are above the ACA subsidy ceiling (above $60,240 for a single adult in 2026), off-exchange PPO is generally the best coverage option.

When is open enrollment for Texas health insurance in 2026?

The HealthCare.gov open enrollment period for 2026 Texas health insurance coverage runs from November 1, 2025 through January 15, 2026. Plans selected by December 15 take effect January 1, 2026; plans selected between December 16 and January 15 take effect February 1, 2026. Outside open enrollment, Texans can enroll or switch HealthCare.gov plans only through a qualifying Special Enrollment Period triggered by a life event — job loss, marriage, divorce, birth, adoption, moving to a new rating area, or losing other coverage — within 60 days of the event. Off-exchange ACA-compliant and PPO plans are available year-round with no open enrollment restriction.

Get Your 2026 Texas Health Insurance Quote

A licensed Texas broker compares all 2026 options — HealthCare.gov marketplace plans by rating area, off-exchange PPO products, CHIP for children, and state retiree programs — with full APTC and CSR subsidy calculation. Free, no obligation, covering all 26 Texas rating areas.

Free Texas health insurance comparison — every coverage path in one call.

Texas Health Insurance Coverage Guides

HealthCare.gov enrollment guide for Texas — APTC subsidies, open enrollment, and SEPs.

Individual Health Insurance TexasIndividual plan options — marketplace, off-exchange PPO, and direct carrier enrollment.

Texas PPO PlansOff-exchange PPO options — BCBSTX, Cigna, UHC compared with Texas hospital network depth.

Self-Employed Health Insurance Texas1099 contractors and sole proprietors — Schedule 1 deduction, HealthCare.gov, and HSA stacking.

Cheap Texas Health InsuranceLowest-cost Texas plans — subsidized Bronze and Silver, CHIP, and affordability ladder by income.

Catastrophic Health Insurance TexasUnder-30 ACA plans — $10,600 deductible, three free PCP visits, hardship exemption pathway.

Short-Term Health Insurance TexasBridge coverage for gap periods — 36-month Texas STLD limit, UHC Golden Rule, BCBSTX, Pivot.

Private Health Insurance TexasOn-exchange vs off-exchange — subsidy trade-off, direct carrier enrollment, COBRA alternatives.

Family Health Insurance TexasCHIP split-enrollment, maternity coverage, family glitch fix, and household cost strategies.

Texas Retiree Health InsurancePre-Medicare bridge ages 55–64 — TRS-Care, ERS, APTC subsidies, COBRA vs marketplace.

Small Business Health Insurance TexasSHOP and group coverage for Texas employers — 1–50 employees, carrier options, tax credits.

PPO Health Insurance PlansNational PPO guide — out-of-network reimbursement, no-referral access, carrier network depth.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Texas residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.